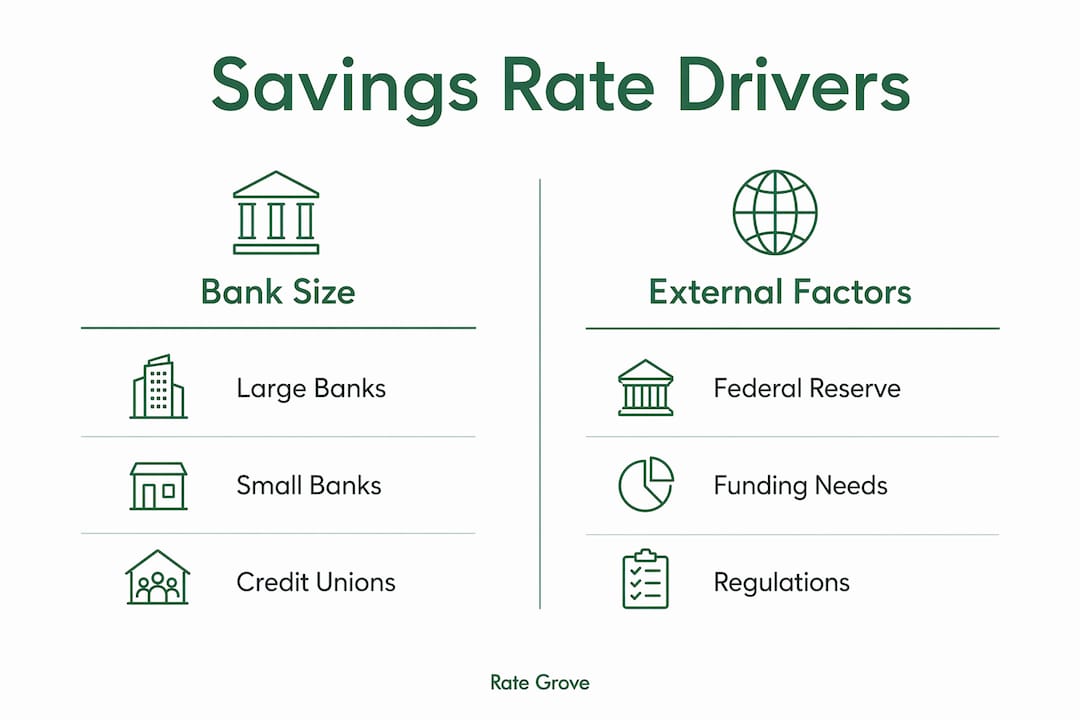

Savings rates differ by bank because each institution sets its annual percentage yield (APY) based on its own funding needs, competitive pressure, and deposit product design. The Federal Reserve influences the broader rate environment, but it does not dictate what any individual bank pays you. Chase may offer 0.01% APY on a standard savings account while an online bank or credit union offers 4% or more on the same type of account. Understanding why savings rates differ by bank puts you in a position to earn significantly more without taking on any additional risk.

Why do savings rates differ by bank?

The core reason for savings account rate differences is that banks price deposits the way any business prices a product: based on supply, demand, and margin. A bank that already holds more deposits than it can profitably lend out has little reason to pay you more. A bank actively growing its loan book needs fresh deposits and will compete for them with a higher APY.

Banks set deposit APYs independently of the Federal Reserve and adjust based on their own funding needs and competitive pressures. That independence is the root cause of bank interest rate variations you see across institutions at any given moment. Two banks operating under the exact same Fed policy regime can offer rates that are miles apart.

This is not a glitch in the system. It is the system working as designed. Deposit pricing is a business decision, not a public utility rate set by a regulator.

How a bank’s funding needs shape the rate it offers you

A bank’s most direct motivation for raising its savings rate is a need for more deposits. Deposits are a bank’s raw material. Without them, it cannot fund mortgages, auto loans, or business credit lines.

When a bank’s lending activity grows faster than its deposit base, it faces a funding gap. To close that gap, it raises savings rates to attract new depositors. The reverse is equally true. Banks flush with cash raise rates slowly and have little incentive to compete aggressively. That dynamic explains why two banks in the same city can offer rates that differ by a full percentage point or more.

Key factors that push a bank to raise its savings rate include:

- A surge in mortgage or commercial loan demand that outpaces deposit growth

- A loss of large institutional depositors who moved funds elsewhere

- A strategic decision to grow market share in a new region

- Pressure from rising funding costs across the broader industry

Pro Tip: Check whether a bank’s savings rate has changed in the past 90 days. Frequent upward adjustments signal that the bank is actively competing for deposits, which tends to favor savers.

Deposit competition typically increases when funding costs plateau or banks need to add or retain depositors, squeezing profit margins. The cost of funding across the industry rose from 2.26% in 2024 to 2.61% in 2025, and renewed competition in 2026 is pushing some banks to raise CD yields to attract longer-term deposits. That pressure benefits savers who shop around.

How the Federal Reserve affects savings rates, and why banks respond differently

The Federal Reserve sets the federal funds rate, which is the rate banks charge each other for overnight loans. That rate sets a floor for borrowing costs across the economy. When the Fed raises rates, banks’ own borrowing costs rise, which generally creates room for higher deposit rates. When the Fed cuts rates, that pressure eases.

The critical point is that banks do not move in lockstep with Fed decisions. Banks adjust variable savings APYs on their own schedules, sometimes daily or monthly, not strictly tied to Fed announcements. Two banks can temporarily invert in their rate rankings despite operating under the same policy environment.

Here is what that means in practice:

- One bank may raise its APY the week after a Fed hike; another may wait three months

- A bank may raise rates by only half the Fed’s increase, pocketing the difference as margin

- A bank may cut rates before the Fed acts if it sees deposit inflows slowing

- Online banks typically respond faster and more fully to Fed increases than large branch networks

The gap between the Fed’s target rate and what your bank pays you is called the “spread.” Large banks historically capture a wide spread. Smaller banks and online institutions tend to pass more of the Fed’s rate changes through to depositors.

Big banks vs. small banks: why size drives rate differences

Bank size is one of the strongest predictors of savings account rate differences. Large banks like Chase operate with enormous, stable deposit bases built over decades. Their customers rarely leave, even when rates are low. That deposit stickiness removes the competitive pressure to raise rates.

Big banks like Chase pay as little as 0.01% APY, while smaller banks and credit unions routinely offer 4% or more. That gap is not accidental. It reflects the fact that large banks rely on stable low-cost deposits to preserve their margins without needing to compete on rate.

| Institution type | Typical APY range | Key driver |

|---|---|---|

| Large national banks | 0.01%–0.50% | Stable deposit base, low competitive pressure |

| Regional banks | 0.50%–3.00% | Moderate competition, mixed funding needs |

| Online banks | 3.50%–5.00%+ | No branch costs, active deposit competition |

| Credit unions | 3.00%–5.00%+ | Member-focused model, lower profit motive |

| Community banks | 2.00%–4.50% | Local competition, targeted deposit growth |

Smaller banks and credit unions operate with thinner deposit cushions. They need to attract new members or customers to fund local lending, so they price their savings products more aggressively. That is a direct benefit to savers who are willing to look beyond their primary checking account bank.

Pro Tip: You do not need to move your checking account to earn a better savings rate. Open a high-yield savings account at a separate online bank and link it to your existing checking. Transfers typically clear in one to two business days.

Understanding how bank fees on small balances interact with low APYs is equally important. A 0.01% APY account that also charges a monthly maintenance fee can cost you money rather than earn it.

How product features and regulations create rate differences

Not all savings accounts are the same product. The terms attached to a deposit account directly affect the rate a bank can offer and still make money. Savings-rate differences reflect product contract terms, including liquidity, withdrawal penalties, and commitment lengths.

Here is how product design drives rate variation:

- Standard savings accounts offer easy access to your money, which means the bank cannot count on those deposits staying put. Lower rate stability for the bank equals a lower rate for you.

- High-yield savings accounts at online banks offer better rates partly because those banks have no branch overhead and partly because they attract rate-sensitive customers who will leave if the rate drops.

- Certificates of deposit (CDs) pay higher rates because you commit your money for a fixed term. The bank gains deposit certainty and passes some of that value back to you as a higher APY.

- Money market accounts often sit between savings and CDs in rate, offering limited check-writing access in exchange for a modest rate premium over standard savings.

Regulatory rules also create a ceiling for some banks. FDIC rate caps limit the maximum deposit rates that less-than-well-capitalized banks can offer. The national rate cap equals the national average rate plus 75 basis points, or 120% of the comparable Treasury yield plus 75 basis points. The local rate cap is set at 90% of the highest rate offered in a given market. These caps prevent struggling banks from using high rates to attract deposits they cannot safely manage.

Many banks also advertise bonus APYs that only apply for a limited time or to a portion of the balance. Some advertised rates are teaser rates that pay the top APY only for the first few months or on balances below a specific threshold. Always verify whether an advertised rate is the ongoing rate or a promotional one before opening an account. Reading bank account fee disclosures carefully will reveal these conditions before you commit.

Key Takeaways

Banks set savings rates based on their own funding needs, competitive position, and product design, not on a single shared standard.

| Point | Details |

|---|---|

| Funding needs drive rates | Banks needing deposits to fund loans offer higher APYs to attract savers. |

| Fed policy is indirect | The Federal Reserve influences the rate environment but does not set individual bank APYs. |

| Size predicts rate | Large banks like Chase pay near zero; online banks and credit unions often pay 4% or more. |

| Product terms matter | CDs pay more than standard savings because you commit your money for a fixed period. |

| Teaser rates mislead | Advertised bonus APYs may apply only for a few months or on limited balance tiers. |

What I’ve learned from watching savings rates across hundreds of banks

After tracking savings rates across a wide range of institutions, the single most common mistake I see is savers comparing advertised rates without reading the fine print. A bank advertising 5.00% APY may be offering that rate only on the first $1,000 or only for the first 90 days. The actual yield on a $10,000 balance over a full year can be a fraction of what the headline suggests.

The second mistake is assuming that a bank offering a great rate today will still offer it in six months. Variable savings rates can change at any time. I have watched banks cut their APYs by a full percentage point within weeks of a Fed rate reduction, while others held their rates steady for months. The banks that hold rates longer tend to be those actively competing for deposit growth, which is worth tracking.

My practical advice: keep your primary checking account where it is convenient, but treat your savings account as a separate, rate-optimized product. The two do not need to be at the same institution. Linking accounts across banks is straightforward at most online banks, and the rate difference between a 0.01% APY account and a 4.50% APY account on a $20,000 balance is roughly $900 per year. That is real money for doing nothing more than opening a second account.

Finally, do not ignore credit unions. They are member-owned, which means profits return to members as better rates and lower fees rather than going to shareholders. Many credit unions now offer online membership open to anyone in the country, removing the old geographic barrier.

— Mat C.

How Rate Grove makes comparing savings rates simple

Finding the best savings rate used to mean visiting a dozen bank websites and manually comparing terms, fees, and APY conditions.

Rate Grove pulls current, verified rate data from bank and regulator sources into one place, so you can compare savings accounts and CDs side by side in minutes. Every listing includes fees, rate conditions, and balance requirements, not just the headline APY. The guides are updated monthly, so you are always looking at current offers rather than rates that expired last quarter. If you want to see which banks are actually competing for your deposits right now, Rate Grove is the fastest way to find out.

FAQ

Why do banks offer such different savings rates?

Banks price savings rates based on their individual funding needs, deposit base stability, and competitive environment. A bank that needs deposits to fund loan growth will offer a higher APY than one already holding excess cash.

Does the Federal Reserve set savings account rates?

The Federal Reserve sets the federal funds rate, which influences borrowing costs broadly, but individual banks set their own savings APYs independently. Banks adjust rates on their own schedules and by their own amounts.

Why do big banks pay lower savings rates than online banks?

Large banks like Chase have stable, loyal customer bases that rarely leave for a better rate. That deposit stickiness removes competitive pressure. Online banks have no branch overhead and actively compete on rate to attract depositors.

What is a teaser rate on a savings account?

A teaser rate is a promotional APY that applies only for a limited period, such as the first three months, or only on balances below a set threshold. Always check whether an advertised rate is the ongoing rate before opening an account.

Can a bank change my savings rate without notice?

Yes. Variable-rate savings accounts allow banks to adjust APYs at any time. Banks are not required to match Federal Reserve moves and can raise or cut rates on their own schedule, sometimes with as little as a few days’ notice.