An introductory rate is a temporary interest rate that banks use as a marketing tool to attract new customers, set deliberately above or below standard rates before reverting to normal pricing. Understanding why banks offer introductory rates helps you separate a genuinely good deal from a short-term illusion. These promotions appear across credit cards, savings accounts, and certificates of deposit, and the mechanics behind them are more calculated than most people realize. Banks like Chase, Marcus by Goldman Sachs, and Ally Bank all use these offers, each with specific terms that determine whether you actually benefit.

Why banks offer introductory rates: the economic logic

Banks offer introductory rates because acquiring a new primary customer is worth far more than the short-term cost of a promotional rate. A one-time acquisition cost of around $300 can generate revenue over ten years through deposits, transactions, and cross-sells. That math makes a temporary 0% APR or elevated savings yield a rational marketing expense, not a giveaway.

The real prize for a bank is not the account you open for the promotion. It is the full relationship that follows. Banks design introductory offers to pull customers into checking accounts, debit cards, auto loans, and mortgages. These products, called relationship anchors, generate far more profit than any single savings rate ever could.

Cross-selling is the engine behind this strategy. A customer who opens a high-yield savings account during a promotion is statistically more likely to consolidate other financial products with the same institution. Banks track this conversion rate carefully, and it justifies the upfront cost of every promotional offer they run.

Pro Tip: If a bank’s introductory offer requires you to open a checking account alongside a savings account, that is not a coincidence. The bank is building a relationship anchor from day one.

Here is what banks gain from introductory rate campaigns:

- New deposit volume: Promotional savings rates attract fresh cash that banks can lend out at higher rates.

- Customer data: New account holders generate behavioral data that banks use to target future product offers.

- Competitive positioning: A visible high APY or 0% APR keeps a bank relevant in rate comparison searches.

- Long-term fee revenue: Checking accounts, overdraft services, and wire transfers generate steady income after the promo ends.

How do introductory rates work across different products?

Introductory rates operate differently depending on the product. The mechanics matter because the risks and rewards are not the same across credit cards, savings accounts, and CDs.

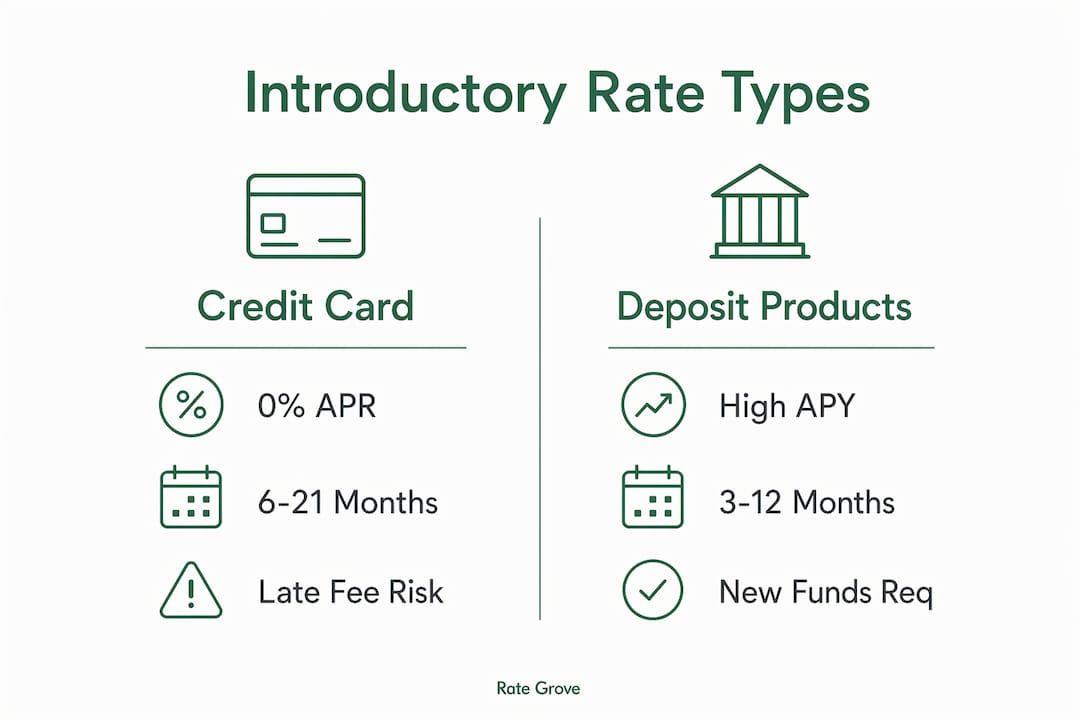

Credit card 0% APR promotions

A credit card introductory APR typically runs for 6 to 21 months, after which a standard variable APR applies. Some offers cover new purchases, others cover balance transfers, and some cover both. The distinction is critical. A balance transfer offer that does not cover new purchases will charge you interest on every new charge from day one.

Losing the promotional rate is easier than most people expect. A single late payment can trigger immediate reversion to the standard APR, which often sits well above 20%. Reading the penalty terms before you transfer a balance is not optional.

Savings account promotional APYs

Deposit products use high promotional APYs to attract new deposits quickly, then drop to lower standard rates after the promo period ends. A common structure is a 5.50% APY for six months that then falls to around 4.00% to 4.25%. That drop is significant if you are counting on a specific return.

Many savings promotions require “new money,” meaning funds that did not previously exist at that bank. This requirement prevents customers from simply moving money between internal accounts to capture the rate. Banks use this rule to grow their actual deposit base, not just shuffle existing funds.

CD promotional rates

A promotional CD rate is fixed for the full term of the certificate. Unlike a savings account, the rate does not drop mid-promotion. The tradeoff is liquidity. You cannot access the funds without an early withdrawal penalty, which can erase the interest you earned.

Here is a quick comparison of how these three products handle introductory rates:

| Product | Typical promo duration | Rate behavior after promo | Key requirement |

|---|---|---|---|

| Credit card (0% APR) | 6–21 months | Reverts to standard variable APR | On-time payments |

| Savings account | 3–12 months | Drops to standard APY | New money deposit |

| CD | Full term (fixed) | No change during term | Minimum deposit, no early withdrawal |

Pro Tip: For savings account promos, set a calendar reminder one month before the promotional period ends. That gives you time to compare rates and move funds if the standard APY is no longer competitive.

What regulations shape introductory rate offers?

Banks do not set promotional rates in a vacuum. FDIC rate caps restrict how far above market rates a bank can pay on deposits, which directly limits how high and how long promotional APYs can run. These caps exist to prevent banks from taking on excessive funding risk by paying unsustainable rates to attract deposits.

Regulatory rate caps also explain why introductory rates are temporary by design. A permanently elevated APY would push a bank above FDIC thresholds, creating compliance risk. The promotional window is the legal and financial ceiling for what a bank can offer without triggering regulatory scrutiny.

Market responsiveness also varies by institution type. Online banks adjust APYs within 24 to 72 hours after Federal Reserve announcements. Traditional brick-and-mortar banks typically lag by 2 to 4 weeks. This means online banks often offer higher promotional rates faster when the Fed raises rates, and they also cut rates faster when the Fed lowers them.

Key regulatory and market factors that shape introductory offers:

- FDIC national rate caps: Set a ceiling on deposit rates relative to market benchmarks.

- Treasury yield benchmarks: Banks price promotional rates relative to current Treasury yields to manage funding costs.

- Liquidity management: Limited-time offers let banks control deposit inflows without committing to permanent high-rate liabilities.

- Consumer protection rules: Regulations require banks to clearly disclose when and how promotional rates change.

What are the real benefits and risks of introductory rates?

The benefits of introductory rates are real, but they are conditional. A 0% APR period on a credit card can save you hundreds of dollars in interest if you pay off a balance before the promo ends. A promotional savings APY can meaningfully boost your returns for six months compared to a standard account paying a fraction of that rate.

The risks are equally concrete. The most common consumer mistake is treating the introductory rate as the permanent rate. Consumers often misunderstand introductory rates as long-term pricing, when the promo period is limited and timing is everything. A savings account that pays 5.50% for six months and then drops to 1.00% is not a high-yield account. It is a six-month promotion attached to a low-yield account.

Behavioral requirements add another layer of risk. Many offers require minimum balances or new money deposits to maintain the promotional rate. Falling below a minimum balance can trigger an immediate rate drop, and the bank is not required to notify you in advance.

Strategies that actually work:

- Time your balance transfer: Move high-interest debt to a 0% APR card and create a payoff plan that clears the balance before the promo ends.

- Use savings promos as a ladder: Open a promotional savings account, earn the elevated APY, then compare rates at expiration and move funds if needed.

- Read the fee disclosures: Understanding bank account fee disclosures before you open an account prevents surprises that can offset any rate benefit.

- Avoid minimum balance traps: If you cannot reliably maintain the required balance, the promotional rate may cost you more in fees than it earns in interest.

How do introductory rates compare to standard bank rates?

Standard savings accounts at large traditional banks currently pay well below what promotional accounts advertise. The gap between a promotional APY and a standard APY at the same institution can be substantial, which is exactly why these offers attract attention.

The more useful comparison is between a promotional account and a flat-rate account with no promotional period. Some online banks offer consistently competitive APYs without a promotional structure. These accounts do not spike high and then drop. They stay at a steady rate that may outperform a promotional account over a full year once the promo period ends.

| Account type | Rate structure | Best for |

|---|---|---|

| Promotional savings account | High APY for 3–12 months, then drops | Short-term savers who will move funds |

| Standard savings account | Low, stable APY | Convenience, not yield |

| Flat-rate high-yield savings | Consistently competitive APY | Long-term savers who want predictability |

| Promotional CD | Fixed rate for full term | Savers who can lock funds away |

When an introductory offer is worth it:

- You have a specific short-term savings goal within the promo window.

- You are carrying high-interest credit card debt and can pay it off during a 0% APR period.

- You are comfortable tracking the expiration date and acting on it.

When it is not worth it:

- You need immediate access to funds and cannot meet minimum balance requirements.

- You tend to set accounts up and forget them, which means you will likely miss the reversion.

- The standard rate after the promo is significantly lower than flat-rate alternatives.

Key takeaways

Banks offer introductory rates as a calculated customer acquisition tool, with the long-term relationship value far exceeding the short-term cost of the promotion.

| Point | Details |

|---|---|

| Introductory rates are temporary | Rates revert to standard pricing after the promo period, often significantly lower or higher. |

| Banks target long-term value | A $300 acquisition cost can generate ten years of revenue through cross-sold products. |

| Product mechanics differ | Credit cards, savings accounts, and CDs each have distinct promo structures and expiration rules. |

| Regulations set the ceiling | FDIC rate caps and Treasury benchmarks prevent banks from offering permanently elevated deposit rates. |

| Timing and terms decide value | Reading the fine print and tracking expiration dates determines whether you actually benefit. |

The part most people skip

Most articles on introductory rates stop at the definition. The part worth paying attention to is the behavioral design underneath these offers. Banks are not being generous. They are making a calculated bet that once you open an account for the promotion, inertia will keep you there long after the rate drops.

I have seen this play out repeatedly. A reader opens a savings account for a 5.50% APY, the rate drops to 1.20% after six months, and they never move the money. The bank wins. The reader loses months of potential earnings. The fix is not to avoid promotional offers. It is to treat every introductory rate like a contract with an expiration date, because that is exactly what it is.

The offers worth taking are the ones where you have a clear plan for what happens on day one after the promo ends. If your plan is “I’ll figure it out later,” the bank has already won. If your plan is “I will compare rates in month five and move funds if needed,” you are using the promotion the way it was designed to be used, just from your side of the table.

One more thing: the small balance fees that often accompany promotional accounts can quietly erase your rate advantage. A $12 monthly fee on an account earning 5.50% APY on a $500 balance means you are paying more in fees than you are earning in interest. Do the math before you open the account, not after.

— Mat C.

Rate Grove makes comparing bank rates straightforward

Sorting through promotional rates across dozens of banks takes time, and the fine print is rarely in your favor. Rate Grove compares CD rates, savings accounts, and credit cards side by side, pulling verified data directly from issuer and regulator sites so you are not working from outdated numbers.

Whether you are looking for the highest promotional APY on a savings account or a 0% APR credit card with the longest intro window, Rate Grove shows you the full picture, including standard rates after the promo ends, fees, and minimum balance requirements. Compare current rates and find the account that actually fits your financial goals, not just the one with the biggest headline number.

FAQ

What is an introductory rate on a bank account?

An introductory rate is a temporary interest rate set above or below standard pricing to attract new customers. It reverts to the standard rate after a defined period, which can range from a few months to over a year.

How long do introductory rates typically last?

Credit card 0% APR offers typically run for 6 to 21 months. Savings account promotional APYs usually last 3 to 12 months. CD promotional rates are fixed for the full term of the certificate.

Can you lose an introductory rate early?

Yes. A late payment on a credit card can trigger immediate reversion to the standard APR. On savings accounts, falling below a minimum balance or failing to meet new money requirements can end the promotion early.

Why do online banks offer higher introductory rates than traditional banks?

Online banks have lower overhead costs and update their rates faster in response to Federal Reserve changes, often within 24 to 72 hours. Traditional banks typically take 2 to 4 weeks to adjust, which means online banks can offer more competitive promotional rates more quickly.

Are introductory rates worth it?

Introductory rates are worth it when you have a clear plan tied to the promo window, such as paying off debt during a 0% APR period or saving toward a short-term goal. Without a plan, the rate drop after the promo ends often outweighs the initial benefit.