Bank fees on small balances are recurring charges that quietly reduce your savings every month, often before you notice the damage. The role of bank fees on small balances is straightforward but costly: monthly maintenance fees, minimum balance penalties, and overdraft charges pull money directly out of accounts that can least afford it. The average monthly maintenance fee for checking accounts ranges from $13.95 to $15.45 in 2026, with large banks charging around $16.35. For someone holding $200 in a checking account, a $15 monthly fee wipes out nearly 10% of their balance in a single billing cycle. Understanding exactly how these charges work is the first step toward stopping them.

What types of bank fees commonly affect small balances?

Several distinct fee types target low-balance accounts, and each one works differently.

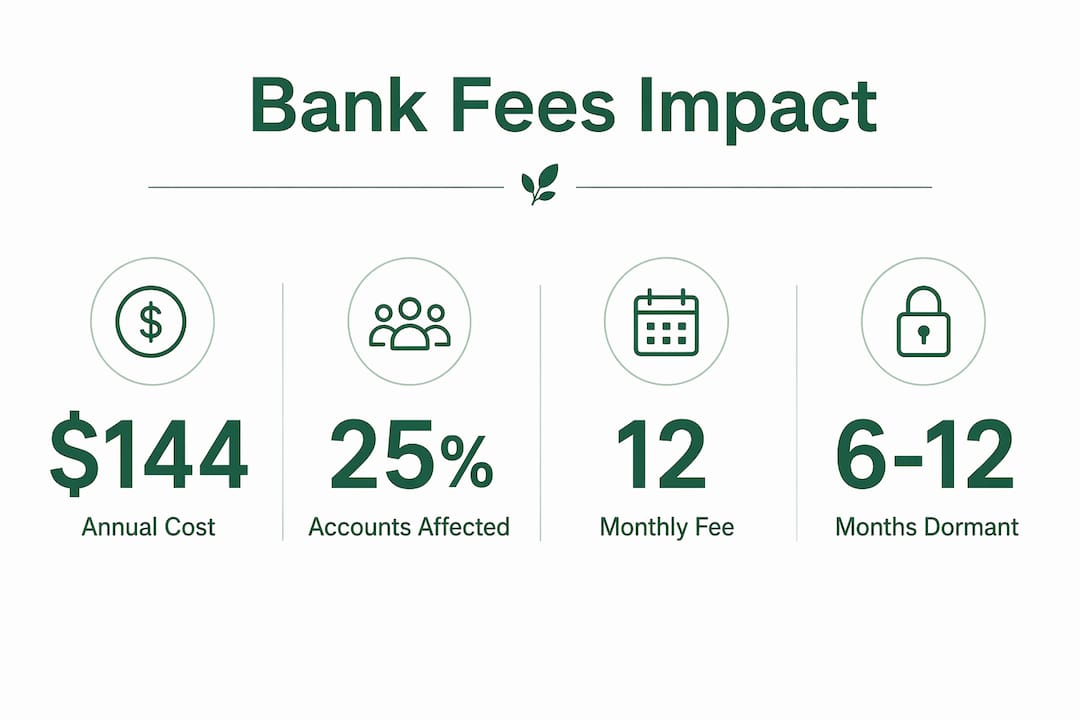

Monthly maintenance fees are the most common. Banks charge these automatically each month simply for holding an account. The average fee at small banks runs around $10.95, while large banks average $16.35. These fees apply regardless of whether you made any transactions.

Minimum balance fees are triggered when your account falls below a set threshold. Approximately 25% of U.S. checking accounts require a minimum balance, with fees between $5 and $25 monthly if you do not maintain it. That means one in four accounts carries this risk.

Overdraft and non-sufficient funds (NSF) fees hit when you spend more than your available balance. U.S. consumers paid an estimated $12.1 billion in overdraft and NSF fees in 2024. Strikingly, 79% of those fees were paid by just 9% of consumers, meaning frequent overdrafters bear the heaviest burden.

Inactivity fees apply when an account sits dormant for a set period, often 6 to 12 months. These are less common but can catch people off guard.

One detail most people miss is how banks measure your balance. Banks calculate minimum balance requirements using your average daily balance across the entire month, not a single snapshot at month’s end. A few low-balance days early in the month can trigger a fee even if your balance looks fine by the 30th.

Pro Tip: Many banks offer combined balance waivers. Balances in linked savings accounts, CDs, or loans at the same institution can count toward your minimum balance threshold, letting you avoid fees without keeping a large sum in any single account.

Why do banks charge fees on small balances?

Banks charge fees on small balances for two main reasons: to cover operational costs and to encourage larger deposits.

Every checking account costs a bank money to maintain. Customer service, fraud monitoring, transaction processing, and regulatory compliance all carry real expenses. Fees help banks recover those costs from accounts that generate little revenue through interest spreads or lending activity.

Minimum balance requirements serve a second purpose. When you keep more money in your account, the bank has more capital available to fund loans and earn interest income. Fees act as a financial nudge to push customers toward higher balances. This model works well for banks but creates a structural disadvantage for anyone who cannot maintain those thresholds.

Industry experts and parliamentary committees have urged banks to stop penalizing customers for not maintaining minimum balances in savings accounts. The argument is that punitive fees push economically vulnerable customers out of the banking system entirely, which harms both individuals and broader financial inclusion goals. A growing number of banks are responding by shifting toward positive reinforcement, such as rewards for consistent deposits, rather than penalties for low balances.

How do bank fees affect savings for vulnerable consumers?

The impact of bank fees falls hardest on consumers who can afford it least.

A $12 monthly fee equals $144 annually, a significant loss for someone with a small balance who could have used that money for essentials or savings growth. That $144 does not just disappear from your account. It also represents lost compounding potential on money that could have earned interest over time.

Racial and economic disparities make this worse. Entry-level checking account fees vary significantly based on neighborhood racial composition, with minority communities often facing higher minimum balance requirements and steeper fees. This pattern reflects a broader systemic issue where fee structures disproportionately burden the communities with the least financial cushion.

The compounding effect is the part most people underestimate. Consider this sequence:

- Month 1: A $15 fee reduces your $300 balance to $285.

- Month 2: Your lower balance makes it harder to meet the minimum threshold.

- Month 3: Another fee hits, and your balance drops further.

- Month 6: You have paid $90 in fees and your balance has shrunk, not grown.

Account maintenance fees function as an automated mechanism that steadily erodes small savings. The erosion is slow enough to feel invisible month to month but significant over a full year.

Pro Tip: Set up free account alerts through your bank’s mobile app. Most major banks, including Chase, Bank of America, and Wells Fargo, let you trigger a text or email when your balance drops below a custom threshold. Catching a low balance before the fee posts can save you money.

How can you minimize bank fees on small accounts?

Minimizing bank fees on small accounts requires choosing the right account type, not just managing your spending more carefully.

Switch to an online bank or credit union

Switching to online banks or credit unions that charge no monthly fees is the most effective long-term strategy for small balance holders. Institutions like Ally Bank, Discover Bank, and many credit unions offer checking accounts with no monthly maintenance fee and no minimum balance requirement. You keep every dollar you deposit.

Use direct deposit to waive fees

Many traditional banks waive monthly maintenance fees if you set up a qualifying direct deposit. The threshold varies by institution but often falls between $250 and $500 per month. If your employer offers direct deposit, this is one of the simplest ways to avoid fees at a traditional bank.

Understand the real cost of maintaining a minimum balance

Keeping $1,500 in a zero-interest checking account to avoid a $12 monthly fee saves you $144 per year. But parking $1,500 in a non-interest-bearing account costs you roughly $60 in foregone interest annually at a 4% APY. The net savings is closer to $84, not $144. That math changes the calculation significantly.

Compare account types side by side

| Account type | Typical monthly fee | Minimum balance required | Best for |

|---|---|---|---|

| Traditional bank checking | $10–$16 | $1,000–$1,500 | Customers with steady income |

| Online bank checking | $0 | $0 | Small balance holders |

| Credit union checking | $0–$5 | $0–$300 | Community-focused savers |

| Student checking | $0 | $0 | Students under 24 |

| Second-chance checking | $5–$15 | $0 | Those rebuilding banking history |

The table makes one thing clear: online banks and credit unions offer the most straightforward path to fee-free banking for anyone with a small balance.

Key takeaways

Bank fees on small balances cost the average consumer $144 or more per year, and switching to a fee-free online bank or credit union is the single most effective way to stop that loss.

| Point | Details |

|---|---|

| Monthly fees add up fast | A $12 monthly fee costs $144 annually, directly reducing small savings. |

| Minimum balance math matters | Keeping $1,500 to avoid a $12 fee saves less than it appears once opportunity cost is factored in. |

| Overdraft fees concentrate on few | 79% of overdraft and NSF fees are paid by just 9% of consumers, making awareness critical. |

| Vulnerable groups pay more | Minority communities face higher minimum balance requirements and steeper fees on average. |

| Online banks eliminate the problem | Fee-free checking at online banks and credit unions removes the fee burden entirely. |

The fee penalty system is overdue for reform

The traditional bank fee model was built for a different era. When physical branches were the only option, maintenance fees made some sense as a cost recovery tool. Today, online banks and credit unions prove that profitable banking does not require charging customers $15 a month for the privilege of holding their own money.

What frustrates me most is the minimum balance trap. Banks frame it as a simple choice: keep enough money in the account and pay nothing. But that framing ignores the reality that people with small balances often cannot maintain $1,500 in a checking account. The fee is not a neutral policy. It is a penalty for being financially stretched.

The shift toward positive reinforcement, rewarding consistent deposits rather than penalizing low balances, is a step in the right direction. But it is moving too slowly. Regulatory pressure and consumer advocacy need to accelerate that change. In the meantime, the most practical advice is to vote with your feet. Move your account to an institution that does not charge you for having a small balance. Online banks and credit unions have made that easier than ever, and the savings are immediate.

— Mat C.

Finding a bank account that works for your balance

If you are carrying a small balance and paying monthly fees, the right account comparison can save you hundreds of dollars a year.

Rategrove makes it simple to compare bank accounts side by side, including fees, minimum balance requirements, and interest rates, all pulled from verified issuer and regulator sources. You can see exactly what each account costs before you open it. Rategrove updates its guides monthly, so the fee data you see reflects current terms, not last year’s numbers. If you want to find a checking or savings account that fits a small balance without the penalty fees, Rategrove is a practical place to start.

FAQ

What is the average monthly bank fee for a checking account?

The average monthly maintenance fee ranges from $13.95 to $15.45 in 2026. Large banks average around $16.35, while smaller banks charge closer to $10.95.

How do bank fees affect savings on small accounts?

A $12 monthly fee costs $144 per year, directly reducing your balance and eliminating money that could have earned interest. Over several years, the compounding loss becomes substantial.

Are small balance fees worth it to avoid?

Yes. Switching to a fee-free online bank or credit union eliminates the fee entirely, which is almost always better than paying $10 to $16 monthly to maintain a traditional account.

How do banks calculate minimum balance fees?

Banks use your average daily balance across the full month, not your balance on a single day. A few low-balance days early in the month can trigger a fee even if your balance recovers later.

What is the fastest way to stop paying bank fees on a small balance?

To link a direct deposit to your account or switch to an online bank with no monthly fee requirement are the two fastest solutions. Credit unions are also worth checking, as many offer free checking with no minimum balance.