Youth account fees are the recurring and one-time charges banks and fintech platforms apply to savings and checking accounts held by minors. Knowing why compare youth account fees matters is the first step to protecting your child’s balance from unnecessary erosion. The average monthly maintenance fee across checking accounts is $13.51, yet nearly 32% of accounts charge nothing at all. That gap is wide enough to make a real difference on a small balance a child is slowly building. Choosing the wrong account can quietly drain savings that should be growing, while the right one can double as a financial classroom.

Why compare youth account fees before opening any account?

Comparing youth account fees is the single most effective way to avoid paying for features your child does not need. Fee structures vary sharply across account types, and the differences compound over months and years. A parent who skips this step often discovers the problem only after a statement shows a balance lower than expected.

The industry term for this category is “minor or custodial accounts,” though most banks market them simply as youth or student accounts. These accounts are governed by the same federal disclosure rules as adult accounts under the Truth in Savings Act, which requires banks to publish all fees clearly. That means the information you need is available. The challenge is knowing where to look and what to compare.

Fee comparisons also reveal which accounts pair low costs with the educational tools children actually benefit from. A no-fee account with no spending visibility teaches nothing. An account with parental controls, goal tracking, and zero monthly charges is the real target. Rate Grove’s bank fee comparison guides are updated monthly and built specifically to help parents cut through that complexity fast.

What types of fees commonly affect youth savings and checking accounts?

Several fee categories show up repeatedly across youth accounts, and each one chips away at a child’s balance in a different way.

- Monthly maintenance fees: The average is $13.51 per month at accounts that charge them. Over a year, that is $162.12 gone before a single transaction. Many youth accounts waive this fee entirely, so paying it is avoidable.

- Out-of-network ATM fees: These average $4.64 per transaction when you combine the bank’s own surcharge with the ATM operator’s fee. A child who withdraws cash twice a month from the wrong machine loses more than $111 per year.

- Overdraft and insufficient funds fees: At an average of $32.75 per occurrence, overdraft fees hit youth accounts especially hard. A small balance can go negative fast, and a single overdraft can wipe out weeks of saving.

- Early account closure fees: Some banks charge $10–$25 if you close an account within 90 to 180 days of opening it. This catches parents off guard when switching to a better option.

- Wire transfer and transaction fees: Accounts with per-transaction limits charge fees once a child exceeds the monthly threshold. These are easy to miss on a fee schedule buried in fine print.

- Inactivity fees: A dormant account can trigger monthly charges after 6 to 12 months of no activity. This is a common surprise for parents who open accounts and then forget to use them regularly.

Pro Tip: Even accounts advertised as “no monthly fee” can carry inactivity fees, per-transaction charges, and ATM surcharges. Always read the full fee disclosure, not just the headline rate.

How do youth account fee structures differ between traditional banks and fintech models?

The two dominant models for youth accounts operate on very different financial logic. Understanding both helps you pick the right fit for your child’s age and your family’s priorities.

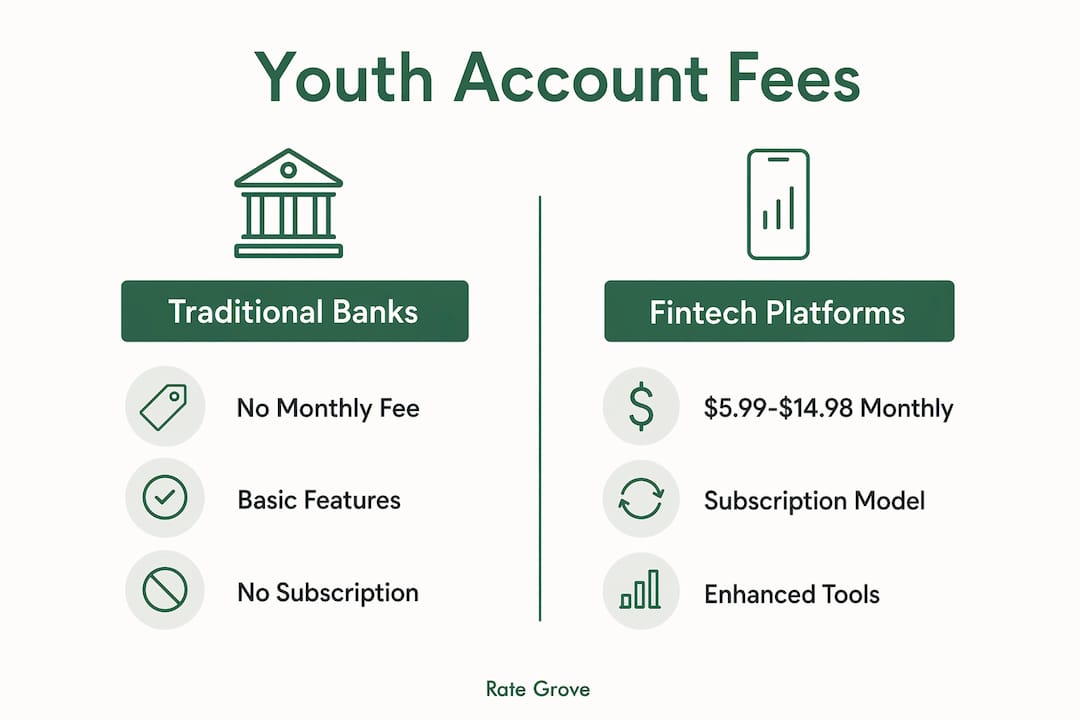

Traditional bank youth accounts typically charge no monthly fee and require no subscription. They are straightforward to open, often linked to a parent’s existing checking account, and covered by FDIC insurance. The trade-off is that most traditional bank apps offer limited budgeting features, no chore tracking, and no visual savings goals built for children.

Fintech subscription accounts flip that model. Subscription fees range from $5.99 to $14.98 per month, but these platforms typically include parental controls, spending categorization, allowance automation, and financial literacy content built into the app. For a parent with a 10-year-old learning to budget, those features have genuine teaching value.

| Feature category | Traditional bank accounts | Fintech subscription accounts |

|---|---|---|

| Monthly fee | $0 (most youth accounts) | $5.99–$14.98/month |

| FDIC insured | Yes | Yes (via partner banks) |

| Parental controls | Basic or none | Advanced, app-based |

| Budgeting tools | Minimal | Goal tracking, chore pay |

| ATM network | Varies by bank | Often limited |

| Overdraft protection | Sometimes available | Usually blocked by design |

The right choice depends on your child’s age and how hands-on you want the financial education to be. For a teenager who already understands basic saving, a no-fee traditional account keeps costs low. For a younger child just starting out, the monthly fee on a fintech platform may be worth the structured learning environment it provides.

Pro Tip: Calculate the annual cost of any subscription account before signing up. A $9.99/month plan costs $119.88 per year. Compare that to what your child’s balance would earn in interest to see if the features justify the price.

What hidden costs should parents watch for when comparing youth account fees?

Hidden fees are the ones that do not appear in the marketing headline. They live in the account agreement, and many parents overlook them entirely until a statement arrives with an unexpected charge.

The most common hidden costs to watch for include:

- Inactivity fees triggered after a set period of no transactions, often 6 to 12 months.

- Early closure fees charged when an account is closed within the first 90 to 180 days.

- Excess transaction fees on savings accounts that limit monthly withdrawals, a holdover from federal Regulation D rules.

- Foreign transaction fees that apply when a child uses a debit card abroad or on international websites.

- Out-of-network ATM fees that apply even on accounts with no monthly maintenance charge.

The most consequential hidden cost is automatic account conversion. Youth accounts convert to standard adult accounts at ages 18–23, depending on the institution. When that conversion happens, the monthly maintenance fee that was waived for minors kicks in automatically. A parent who opened an account for a 14-year-old and forgot about it could find their young adult paying $13.51 per month without realizing it.

Balancing flexibility against restrictions also matters. High-yield savings accounts for kids sometimes limit withdrawals to six per month. That restriction teaches patience but can frustrate a teenager who needs access to funds for school expenses. Read the full fee disclosure before opening any account, and check the conversion policy specifically.

How can comparing youth account fees impact your child’s savings growth?

Fees and savings growth are directly connected. Every dollar paid in fees is a dollar that does not compound. On a small balance typical of a youth account, that effect is proportionally large.

Here is how a thoughtful fee comparison supports both savings and financial learning:

-

Protect compound interest from the start. A $500 balance earning 4% annually grows to $608 over five years with no fees. A $13.51 monthly fee erases that gain entirely and then some. Choosing a no-fee account lets compound interest do its job without interference.

-

Use fee-free accounts as a teaching tool. When a child’s balance grows predictably, it is easier to show them how saving works. Fees create confusion. A statement that shows a lower balance than expected is hard to explain to a 9-year-old. Fee-free accounts simplify compound interest learning by removing that noise.

-

Match account features to your child’s financial stage. A 7-year-old benefits from visual savings goals and parental approval on spending. A 16-year-old benefits from a real debit card with spending limits and no overdraft risk. The right account at the right age reinforces good habits rather than creating friction.

-

Avoid overdraft fees by design. Many youth-focused accounts block overdrafts entirely, which means a declined transaction instead of a $32.75 fee. That design choice alone can save a family significant money over the life of the account.

-

Review accounts as your child grows. An account that was perfect at age 10 may be the wrong fit at 15. Balancing cost and flexibility means revisiting the account annually and switching when a better option exists. Rate Grove’s guide on small balance fees shows exactly how this erosion plays out in real numbers.

Key Takeaways

Comparing youth account fees before opening any account is the most direct way to protect your child’s savings and build genuine financial literacy from an early age.

| Point | Details |

|---|---|

| Monthly fees add up fast | At $13.51/month, a fee-charging account costs over $162 per year on a small balance. |

| Hidden fees are the real trap | Inactivity, early closure, and ATM fees appear even on “no monthly fee” accounts. |

| Fintech costs more upfront | Subscription accounts run $5.99–$14.98/month but offer stronger educational tools. |

| Account conversion triggers fees | Youth accounts auto-convert to adult accounts at 18–23, often activating new charges. |

| Fee-free accounts teach better | Removing fee noise makes it easier for children to see how saving and compounding work. |

Why I think most parents underestimate this decision

Parents tend to treat the youth account choice as a one-time administrative task. Open it, fund it, move on. I have seen that approach cost families real money over time, and the loss is almost always invisible until it is too late to undo.

The part that surprises most parents is not the monthly maintenance fee. They know to look for that. What catches them off guard is the combination of smaller charges: an ATM fee here, an inactivity charge there, and then a conversion to an adult account at 18 that nobody noticed. Those costs do not feel significant individually. Together, they can erase a year or more of a child’s savings progress.

My honest recommendation is to treat this like any other financial decision you would research carefully. The educational value of fee-free accounts is real, and it compounds just like interest does. A child who watches their balance grow without mysterious deductions learns that saving works. That lesson is worth more than any app feature a subscription account offers.

Check the account again every year. Children’s needs change, and so do the products available to them. The best account at age 8 is rarely the best account at age 14.

— Mat C.

Rate Grove makes youth account comparisons simple

Finding the right youth account used to mean visiting multiple bank websites, reading dense fee disclosures, and hoping you caught everything. Rate Grove removes that friction entirely.

Rate Grove’s bank and account comparison tool pulls verified fee data directly from issuer and regulator sources, so you are always working with current numbers. The guides are fact-checked and updated monthly, which matters in a market where fee structures change without much notice. Whether you are comparing a traditional bank youth account against a fintech subscription model, or checking whether a no-fee account actually has no fees, Rate Grove gives you a clear side-by-side view in minutes. No outdated information, no guesswork, and no need to read five different fee schedules to get a straight answer.

FAQ

What is the average monthly fee for a youth checking account?

The average monthly maintenance fee across checking accounts is $13.51, though many youth accounts waive this fee entirely. Nearly 32% of checking accounts charge no monthly maintenance fee at all.

Do no-fee youth accounts really have no fees?

No-fee youth accounts eliminate the monthly maintenance charge but can still carry inactivity fees, out-of-network ATM fees, and early closure fees. Always read the full fee disclosure before opening an account.

When do youth accounts convert to adult accounts?

Most youth and student accounts convert automatically to standard adult accounts when the account holder reaches ages 18–23, depending on the bank. That conversion often activates monthly maintenance fees that were previously waived.

Are fintech subscription accounts worth the monthly cost?

Fintech accounts charging $5.99–$14.98 per month offer stronger parental controls and financial education tools than most traditional bank accounts. Whether the cost is worth it depends on your child’s age and how much you plan to use those features.

How do fees affect a child’s savings growth?

Fees reduce the balance available to earn interest, which shrinks the compounding effect over time. On a small youth account balance, even a modest monthly fee can erase annual interest earnings entirely.