Comparing CD rates is the single most effective savings habit a freelancer can build. A certificate of deposit (CD) is a fixed-term savings account that pays a guaranteed interest rate in exchange for locking up your money for a set period. The gap between what your primary bank offers and what the best institutions pay can exceed 3 percentage points, which translates to $450 more per year on a $25,000 deposit. That difference matters even more for freelancers, whose irregular income makes every dollar of passive yield count. Understanding why freelancers compare CD rates starts with knowing how wide that gap actually is.

Why freelancers compare CD rates across institutions

The rate spread between major national banks and top-paying institutions is not a small rounding error. National average CD rates often misrepresent real earning potential, because they blend the low offers from large brick-and-mortar banks with the higher yields from online banks and credit unions. Sticking with your default bank means accepting a rate that may be far below what the market actually offers.

Online banks carry lower overhead than traditional branches. That cost savings gets passed directly to depositors in the form of higher APYs. Credit unions, which are member-owned nonprofits, also tend to offer above-average rates because they are not focused on generating profit for shareholders. Understanding why savings rates differ by institution type is the first step toward capturing better yields.

Here is what drives rate differences across institutions:

- Funding needs: Banks actively competing for deposits raise rates to attract new money. A bank flush with deposits has no incentive to offer top rates.

- Overhead costs: Online banks with no physical branches pass their savings to depositors through higher yields.

- Promotional rates: Some institutions offer limited-time rates to hit deposit targets. These windows close fast.

- Regulatory structure: Credit unions operate under different rules than commercial banks, which often allows them to offer more competitive rates.

Pro Tip: Search beyond your primary bank before opening any CD. The best rates almost always come from online banks or credit unions, not the institution where you keep your checking account.

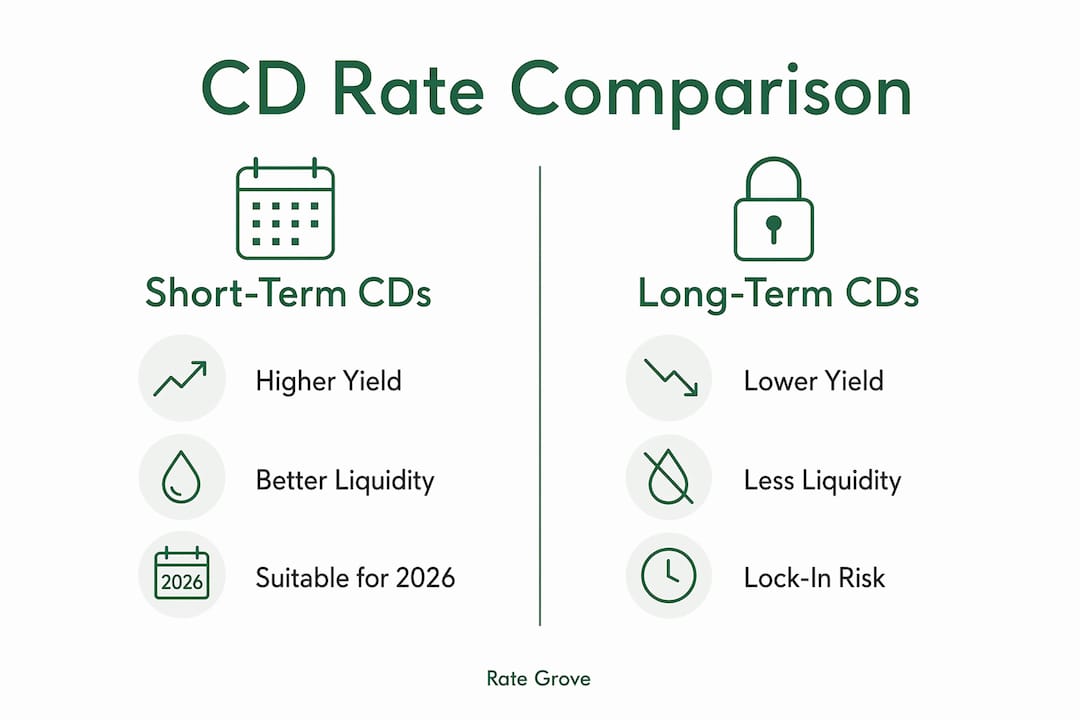

How does the 2026 inverted yield curve affect CD term choices?

The CD yield curve is inverted in 2026, which means shorter-term CDs pay more than longer-term ones. This flips the traditional assumption that locking your money away for five years earns the best return. The inversion reflects market expectations that the Federal Reserve will cut interest rates in the future, so banks are not willing to commit to high long-term rates.

For freelancers, this changes the math on term selection entirely. Choosing a 5-year CD right now could lock you into a lower rate than a 6-month or 12-month CD offers today. The inverted yield curve rewards shorter commitments, which also happens to suit freelancers better given their need for periodic access to funds.

| CD Term | Typical Yield Curve (Normal) | 2026 Inverted Curve |

|---|---|---|

| 6 months | Lower yield | Higher yield |

| 12 months | Moderate yield | Higher yield |

| 3 years | Higher yield | Moderate yield |

| 5 years | Highest yield | Lower yield |

The practical takeaway is clear. A 6-month or 12-month CD currently delivers more interest than a 5-year CD, with far less commitment. Freelancers who need flexibility can roll over short-term CDs as rates evolve, rather than locking into a long-term product that underperforms. Checking fixed vs. variable CD structures helps you decide which term and rate type fits your cash flow timeline.

Why is liquidity management crucial for freelancers investing in CDs?

Freelancers face income variability that salaried workers do not. A slow month can arrive without warning, and a CD with an early withdrawal penalty is the wrong place to keep money you might need next week. The right approach treats CDs as yield enhancers for surplus funds, not as a substitute for an emergency reserve.

Freelancers should keep 6 to 12 months of essential expenses in liquid accounts before moving any money into a CD. That liquid buffer covers rent, utilities, insurance, and other fixed costs during a slow period without forcing you to break a CD early. Only funds beyond that buffer belong in a CD.

A layered savings structure works well for most freelancers:

- Tier 1: Operating account. Cover one to two months of expenses in a checking account for day-to-day cash flow.

- Tier 2: Liquid emergency fund. Keep 6 to 12 months of expenses in a high-yield savings account. This money stays accessible with no penalty.

- Tier 3: CD ladder. Place surplus funds into CDs of staggered terms. As each CD matures, you can reinvest or access the cash depending on your situation.

This income smoothing approach keeps you protected during slow months while still putting idle money to work. Early withdrawal penalties can range from 3 to 12 months of interest depending on the institution and term, so breaking a CD early can wipe out a significant portion of your earnings.

Pro Tip: Build your CD ladder using short-term CDs in 2026. Given the inverted yield curve, 6-month and 12-month terms pay more and mature faster, giving you regular opportunities to reassess rates or access funds.

What factors beyond APY should freelancers consider when comparing CDs?

The headline APY is the starting point, not the finish line. Several other factors determine your actual return, and missing any one of them can cost you money or create unexpected problems.

- APY vs. nominal rate: APY accounts for compounding frequency, while the nominal rate does not. Daily compounding produces a higher effective return than monthly compounding at the same stated rate. Always compare APYs, not nominal rates.

- Minimum deposit requirements: Minimums vary from $500 to over $100,000 depending on the institution. A high-rate CD with a $25,000 minimum is irrelevant if your surplus funds total $5,000.

- Early withdrawal penalties: These can range from 3 to 12 months of interest depending on the term and institution. A penalty that large can eliminate your earnings entirely if you need to exit early.

- Tax treatment: CD interest is taxable as ordinary income and reported on Form 1099-INT, even if you reinvest it rather than withdraw it. Freelancers who pay quarterly estimated taxes need to factor this into their tax planning.

- FDIC or NCUA insurance: Confirm that any institution you use carries federal deposit insurance. FDIC covers banks up to $250,000 per depositor; NCUA provides equivalent coverage for credit unions.

Comparing these factors side by side across multiple institutions is the only way to identify the CD that delivers the best real return for your specific situation.

Key Takeaways

Freelancers who compare CD rates across institutions consistently earn more than those who default to their primary bank’s offer.

| Point | Details |

|---|---|

| Rate spreads are large | The gap between top offers and average bank rates can exceed 3 percentage points, worth $450 more per year on $25,000. |

| Short terms win in 2026 | The inverted yield curve means 6-month and 12-month CDs currently pay more than 5-year CDs. |

| Liquidity comes first | Keep 6 to 12 months of expenses in liquid accounts before putting any surplus into a CD. |

| APY beats nominal rate | Always compare APYs, not stated interest rates, because compounding frequency changes your actual return. |

| Penalties and taxes matter | Early withdrawal penalties can erase months of interest, and CD earnings are taxable as ordinary income each year. |

The habit most freelancers skip

I have watched freelancers spend hours negotiating a client contract for an extra $200, then open a CD at their default bank without checking a single alternative. The math on that choice is painful. Settling for a 2.7% APY when a 4.5% APY is available on the same term and deposit size is not a minor oversight. It is a decision that costs real money every year.

The freelance income model makes this comparison even more critical than it is for salaried workers. You do not have an employer contributing to a 401(k) or smoothing out your monthly cash flow. Every savings decision you make carries more weight. The CD you choose for your surplus funds is one of the few places where doing 20 minutes of research has a direct, guaranteed payoff.

The 2026 inverted yield curve adds another layer that most general savings advice ignores. Conventional wisdom says longer terms earn more. Right now, that is simply wrong. A freelancer who locks into a 5-year CD today based on outdated assumptions will underperform someone who chose a 12-month CD and plans to reassess. Staying current on rate structures is not optional. It is part of managing your finances well.

My honest recommendation is to treat CD rate comparison as a recurring task, not a one-time event. Rates shift. Your surplus funds change. The yield curve will eventually normalize. Reviewing your options every time a CD matures takes less than 30 minutes and consistently produces better outcomes than autopilot.

— Mat C.

How Rate Grove helps freelancers find better CD rates

Freelancers need current, accurate data to make good savings decisions. Rate Grove compares CD rates across banks, credit unions, and online institutions using verified data from issuer and regulator sites, updated monthly.

Every comparison on Rate Grove shows APY, minimum deposit requirements, term length, and penalty terms side by side. You get the full picture without hunting across a dozen bank websites. Whether you are building a CD ladder or placing a single deposit, compare CD rates on Rate Grove to find the best available offer for your situation. The platform is free to use and built for readers who want clear answers fast.

FAQ

Why do freelancers compare CD rates more carefully than salaried workers?

Freelancers manage irregular income without employer benefits, so every savings decision carries more weight. A higher CD rate directly increases passive income with no additional work required.

What is the benefit of comparing CD rates across multiple institutions?

The rate spread between institutions can exceed 3 percentage points, meaning a freelancer with $25,000 could earn $450 more per year simply by choosing the right bank.

Should freelancers choose short-term or long-term CDs in 2026?

Short-term CDs of 6 to 12 months currently pay higher rates due to the inverted yield curve. Longer terms offer lower yields and less flexibility for freelancers with variable cash flow.

How much should a freelancer keep outside of CDs?

Freelancers should keep 6 to 12 months of essential expenses in liquid accounts before placing any surplus into a CD. This buffer protects against slow months without triggering early withdrawal penalties.

Is CD interest taxable for self-employed freelancers?

CD interest is taxable as ordinary income every year, reported on Form 1099-INT, regardless of whether you withdraw it or reinvest it. Freelancers paying quarterly estimated taxes should account for this income each quarter.