Credit card fees are defined as charges applied at multiple points in a transaction, split among card networks, issuing banks, and payment processors. Understanding why credit card fees vary is the first step to making smarter choices about which cards you carry and how you use them. The fee you pay or absorb depends on the card type, how the transaction is processed, the merchant’s industry classification, and the network handling the payment. These factors combine in ways that can push total processing costs anywhere from well under 2% to well over 3% per transaction.

Why credit card fees vary: the three-part fee structure

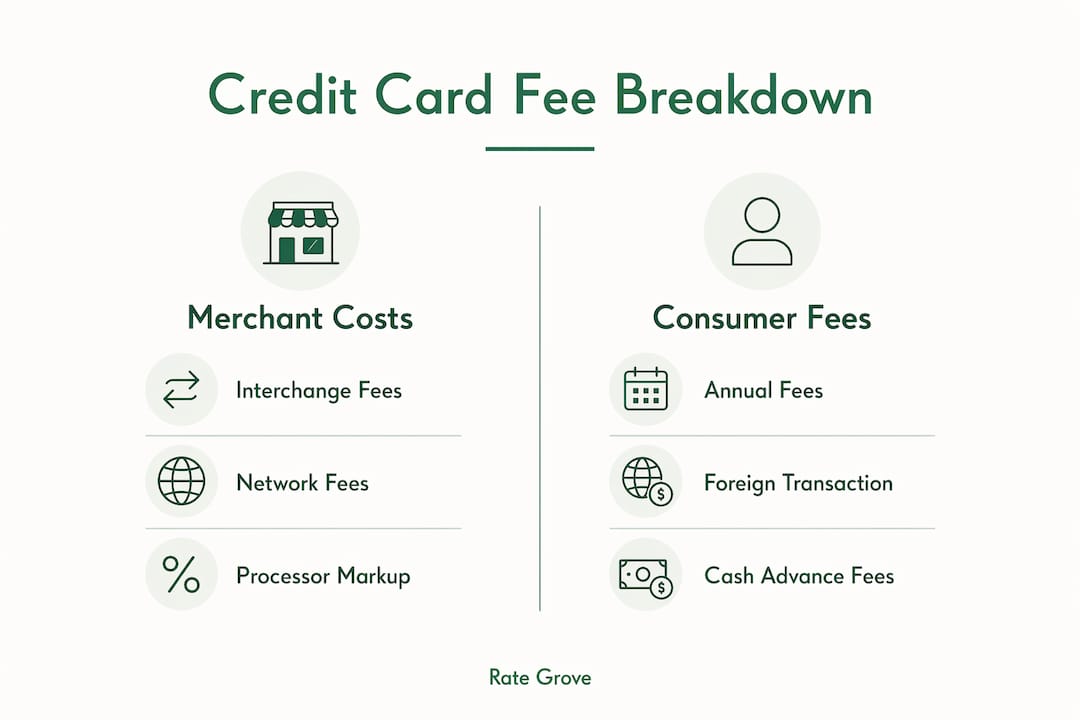

Every credit card transaction carries three distinct cost layers. Merchants pay 1.5%–3.5% per transaction on average, with interchange fees making up 70%–90% of that total. That single fact explains why most fee conversations start and end with interchange. Network assessment fees add another 0.13%–0.25% on top, and the processor markup covers the rest. Knowing which layer is negotiable and which is fixed gives you real leverage.

Interchange fees are set by card networks like Visa and Mastercard and paid directly to the issuing bank. They are non-negotiable. No merchant or consumer can change them. Processor markups, on the other hand, are fully negotiable and represent the only part of the fee stack where you can push back. Understanding this distinction is the foundation of any cost-effective credit management strategy.

What are interchange fees and how do card types affect them?

Interchange fees are the largest single component of credit card processing costs, and they shift significantly based on the type of card used. Standard consumer cards carry the lowest rates. Rewards cards and premium cards carry higher rates because the issuing bank uses that revenue to fund cashback, points, and travel perks.

Card type determines interchange rates in a predictable pattern:

- Standard cards: approximately 1.51% + $0.10 per transaction

- Rewards cards: approximately 1.65%–1.80% + $0.10 per transaction

- Premium cards: approximately 2.10%–2.40% + $0.10 per transaction

The fixed dollar component ($0.10) matters more on small purchases. A $5 coffee charged to a premium card can carry an effective rate well above 4% once you factor in that flat fee. For high-volume, low-ticket merchants like coffee shops or fast-food restaurants, card type differences add up fast.

Premium cards cost more to process because the issuing bank takes on greater fraud liability and funds richer rewards programs. The merchant absorbs that cost every time a customer swipes a Visa Infinite or a World Elite Mastercard. This is why some small businesses post minimum purchase requirements for card payments.

Pro Tip: If you run a business, ask your processor to break out interchange fees by card type in your monthly statement. You may find that a disproportionate share of your costs comes from a small number of premium card transactions.

How does the transaction method change what you pay?

The way a card is used changes the fraud risk profile of the transaction, and that risk gets priced directly into the fee. Card-present transactions, where the physical card is tapped, swiped, or inserted at a terminal, carry the lowest fraud risk. Card-not-present transactions, such as online purchases, phone orders, or manually keyed entries, carry significantly higher risk.

Card-not-present transactions cost roughly 2–3 times more in fees than card-present transactions. That gap exists because the issuing bank cannot verify the physical card or the cardholder’s identity with the same confidence. Higher fraud exposure means higher interchange rates to compensate.

| Transaction method | Relative fraud risk | Fee impact |

|---|---|---|

| Chip insert (EMV) | Low | Lowest interchange rate |

| Contactless tap | Low | Lowest interchange rate |

| Magnetic stripe swipe | Medium | Slightly higher rate |

| Online (card-not-present) | High | Significantly higher rate |

| Phone or keyed entry | High | Highest rate tier |

Debit cards follow a different set of rules. Regulated debit cards issued by banks with assets over $10 billion fall under the Durbin Amendment, which caps interchange at approximately 0.05% + $0.22 per transaction. That cap makes debit transactions far cheaper for merchants than most credit card transactions. Unregulated debit cards from smaller banks are not subject to the same cap and can carry rates closer to standard credit card levels.

Pro Tip: If your business takes a high volume of online orders, ask your processor about address verification service (AVS) tools. Using AVS can reduce your card-not-present fraud rate and may qualify you for lower interchange tiers.

How does merchant category affect credit card fees?

Every business that accepts credit cards is assigned a Merchant Category Code, or MCC. Card networks use the MCC to classify the type of business and assign the appropriate interchange rate. MCC classification directly affects the interchange rate a merchant pays, regardless of the business’s actual risk profile.

High-risk MCCs, such as those assigned to travel agencies, online gambling platforms, or certain subscription services, carry higher interchange rates. Low-risk MCCs, such as grocery stores or utilities, often qualify for preferential rates. A business misclassified into a high-risk MCC pays inflated fees on every single transaction, even if its actual chargeback rate is near zero.

Several factors beyond MCC also shape what a merchant pays:

- Business size and volume: Higher monthly processing volume often qualifies a business for lower negotiated rates with processors.

- Average ticket size: Businesses with large average transactions pay less in percentage terms relative to the fixed per-transaction fee.

- Industry regulations: Some states prohibit surcharging customers to recover credit card fees, so merchants in those states must absorb the full cost.

- Chargeback history: A high chargeback ratio can push a merchant into a higher-risk category over time.

Verifying your MCC with your acquiring bank is a practical step that many business owners skip. A misclassification can cost thousands of dollars annually in unnecessary fees. You can request an MCC review if you believe your classification does not match your actual business type.

What fees do consumers pay directly on their credit cards?

Credit card fee differences are not only a merchant problem. Consumers face their own set of charges that vary widely depending on the card and how it is used. Common consumer fees in 2026 include:

- Annual fees: $0 to $500 or more, depending on card tier and rewards program

- Balance transfer fees: 3%–5% of the transferred amount

- Cash advance fees: 3%–5% of the advance, plus a minimum dollar amount

- Foreign transaction fees: 2%–3% of each international purchase

Annual fees are the most visible cost. A no-fee card is not always the cheapest option if it carries a higher APR or fewer protections. A $95 annual fee card that earns $200 in rewards annually still comes out ahead. The math depends entirely on your spending habits and how you use the card.

Foreign transaction fees are easy to overlook until you get your statement after an international trip. Many travel-focused cards waive this fee entirely. If you travel even once or twice a year, choosing a card without foreign transaction fees is one of the simplest ways to cut costs. Learning to read fee disclosures before you apply saves you from surprises later.

Balance transfer and cash advance fees apply only when you use those specific features. Avoiding cash advances entirely is the cleanest solution, since they also typically start accruing interest immediately with no grace period.

How do payment processors and network fees add to the total?

Network assessment fees are charged by Visa, Mastercard, and other card brands on every transaction. These fees range from 0.13% to 0.25% and are non-negotiable. Every merchant pays them at the same rate. They fund the card network’s infrastructure, fraud monitoring, and brand operations.

Processor markup is the fee your payment processor charges on top of interchange and network fees. Only the processor markup is negotiable, and it covers services like payment terminals, customer support, and compliance tools. This is where merchants have real room to save money by shopping around or renegotiating contracts.

Pricing model transparency matters as much as the rate itself. Interchange-plus pricing separates the interchange fee from the processor markup clearly on every statement. Tiered pricing bundles fees into broad categories and is typically less transparent and less cost-effective. With tiered pricing, you often cannot tell whether a transaction was processed at the qualified, mid-qualified, or non-qualified rate, which makes it harder to identify where costs are rising.

Pro Tip: Ask any processor you are evaluating to quote you on an interchange-plus basis. If they refuse or cannot provide a clear breakdown, that is a signal to keep shopping.

Key takeaways

Credit card fees vary because of a layered structure involving interchange rates, card type, transaction method, merchant classification, and processor pricing, and only the processor markup is negotiable.

| Point | Details |

|---|---|

| Interchange is the biggest cost | Interchange fees make up 70%–90% of total processing costs and are set by card networks. |

| Card type drives rate differences | Premium and rewards cards carry higher interchange rates to fund benefits and cover fraud risk. |

| Transaction method changes risk pricing | Card-not-present transactions cost 2–3 times more than card-present due to higher fraud exposure. |

| MCC classification affects merchant fees | A wrong MCC can inflate fees for low-risk businesses; verifying your code is worth the effort. |

| Processor markup is the only negotiable fee | Choosing interchange-plus pricing and negotiating markup are the most direct ways to cut costs. |

The fee structure rewards the informed

Most people treat credit card fees as a fixed cost of doing business or a hidden tax on spending. I have spent years watching both consumers and small business owners overpay because they assumed the fee was the fee and nothing could be done about it. That assumption is expensive.

The part that surprises people most is how much card type matters on the merchant side. A customer paying with a premium travel card is genuinely costing a small retailer more than a customer paying with a basic debit card. That is not a policy failure. It is the direct result of how interchange funds rewards programs. Once you understand that, you stop being surprised by minimum purchase signs at small businesses.

For consumers, the biggest mistake I see is ignoring annual fees and foreign transaction fees when choosing a card. A card with a $0 annual fee is not automatically cheaper. If it carries a 3% foreign transaction fee and you travel internationally, you can easily pay more than the cost of a premium travel card with no foreign transaction fee. The right card for your habits is the cheapest card, not the one with the lowest sticker price.

The one thing I consistently recommend: read the Schumer Box before you apply. Every credit card is required to disclose its fees in a standardized format. It takes two minutes and tells you everything you need to know about what you are agreeing to.

— Mat C.

Rate Grove makes credit card fee comparisons straightforward

Sorting through credit card fee structures on your own takes time and patience. Rate Grove pulls verified fee data directly from issuer and regulator sites, then presents it in a side-by-side format so you can see annual fees, foreign transaction fees, and rate differences without digging through fine print.

Whether you are looking for a no-fee everyday card or a travel card that offsets its annual cost, Rate Grove’s monthly-updated guides give you current, fact-checked numbers. Compare credit cards and rates at Rate Grove to find the option that fits your spending habits and keeps your costs low.

FAQ

What is the main reason credit card fees vary?

Credit card fees vary primarily because of interchange rates, which differ by card type, transaction method, and merchant category. These rates are set by card networks and are non-negotiable for merchants.

Are any credit card processing fees negotiable?

Only the processor markup is negotiable. Interchange fees and network assessment fees are fixed by card networks and cannot be changed by merchants or consumers.

Why do rewards cards cost merchants more to process?

Rewards cards carry higher interchange rates because the issuing bank uses that revenue to fund cashback, points, and travel benefits. Premium card rates typically range from 2.10%–2.40% plus a fixed per-transaction fee.

What is a Merchant Category Code and why does it matter?

A Merchant Category Code (MCC) is a four-digit number assigned to every business that accepts credit cards. It determines which interchange rate applies, so a misclassified MCC can result in higher fees even for low-risk businesses.

How can consumers reduce the fees they pay on credit cards?

Consumers can reduce fees by choosing cards with no annual fee or no foreign transaction fee based on their usage, avoiding cash advances, and comparing card options before applying to find the best fit for their spending patterns.