Credit card comparison is defined as the structured, side-by-side evaluation of multiple credit card offers to identify the best fit based on fees, interest rates, rewards, and credit requirements. Financial experts consistently recommend this process as the most reliable way to avoid overpaying and to match a card to your actual spending habits. Tools can track over 1,500+ offers, giving you a broad view of the market rather than a narrow look at whatever a bank happens to promote. Understanding credit card comparisons at this level transforms a confusing decision into a clear, data-driven one.

What does credit card comparison mean in practice?

Credit card comparison, also called offer evaluation or card benchmarking in personal finance circles, means measuring multiple cards against the same set of criteria at the same time. You are not just reading one card’s brochure. You are placing several offers next to each other and scoring them on the factors that matter most to your situation.

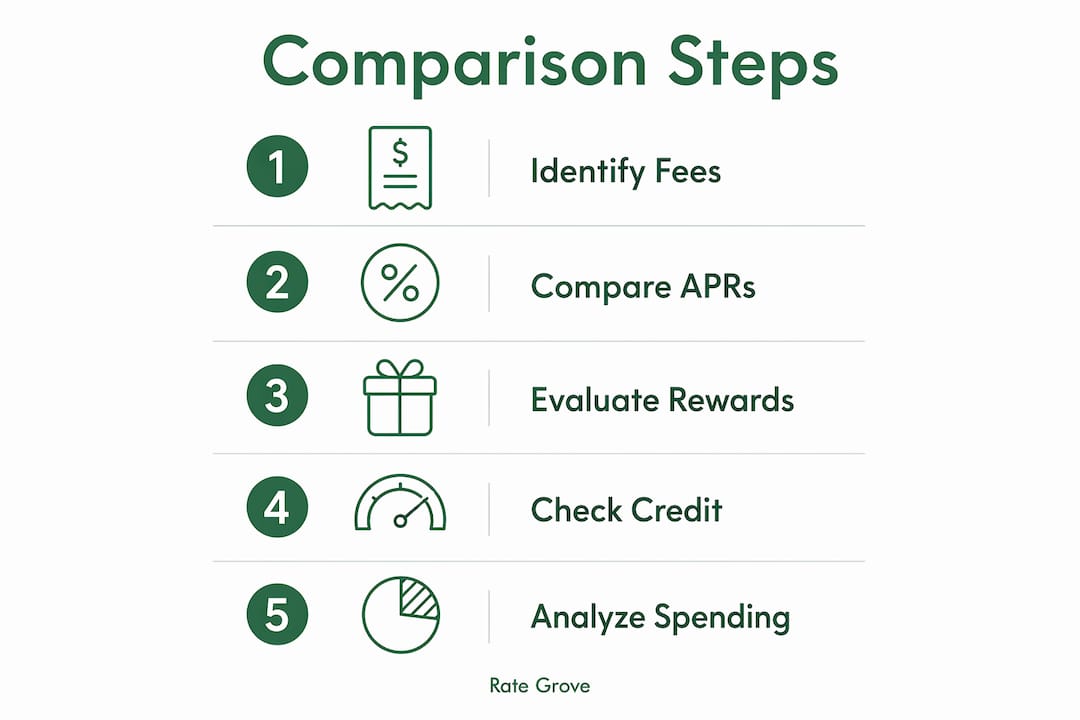

The core criteria fall into four categories: fees, interest rates, rewards, and credit requirements. Each one affects your total cost or benefit in a different way. Skipping even one category produces an incomplete picture and can lead to a poor choice.

A credit card comparison guide built around these four pillars gives you a repeatable framework. You can use it every time you consider a new card, not just once.

What factors are essential when comparing credit cards?

Fees: the costs you pay regardless of behavior

Annual fees for premium cards typically range from $95 to $550. Foreign transaction fees add 1%–3% on purchases made abroad. Late payment fees reach up to $40. Cash advance fees and balance transfer fees layer on additional costs that most cardholders underestimate.

The total fee picture matters more than any single charge. A card with a $550 annual fee can still deliver net value if its travel credits and rewards outpace that cost. A card with no annual fee can still cost you money through foreign transaction fees alone if you travel regularly.

- Annual fee: $0 to $550+ depending on card tier

- Foreign transaction fee: typically 1%–3% per transaction

- Balance transfer fee: usually 3%–5% of the transferred amount

- Late payment fee: up to $40 per occurrence

- Cash advance fee: often 3%–5% with no grace period

Pro Tip: Read the fee schedule in the Schumer Box, the standardized disclosure table required on every credit card offer. It lists all fees in one place and is far more reliable than the marketing summary.

Interest rates: the number that matters most if you carry a balance

The average credit card APR as of may 2026 is 19.19%. That benchmark tells you whether a card’s rate is competitive or expensive. Lower APRs generally require excellent credit.

A single card carries multiple APRs depending on the transaction type. Purchase APR, balance transfer APR, cash advance APR, and penalty APR can all differ significantly on the same card. Most people only notice the purchase APR and miss the others entirely.

Rewards: read past the headline rate

Rewards programs advertise their best-case numbers. A card that promises 5% back on groceries may cap that rate at $6,000 in annual spending, then drop to 1% after that. Rewards rates can be misleading without accounting for spending caps and category restrictions.

The net benefit calculation is straightforward: project your realistic annual rewards, then subtract the annual fee. The result is your true gain from the card.

Credit requirements: know your tier before you apply

Credit score awareness is key when selecting cards. Applying to a card designed for excellent credit when your score is in the fair range wastes an application and triggers a hard inquiry that temporarily lowers your score. Focusing your comparison on cards within your credit tier protects your score and raises your approval odds.

How do personal spending habits influence credit card comparison?

Your spending patterns are the filter that turns a general comparison into a personal one. A card that ranks highly for frequent flyers may rank poorly for someone who rarely travels. The benefits of credit card comparison only materialize when you match the card’s reward structure to your actual behavior.

Follow these steps to align your habits with your comparison:

- Pull three to six months of bank and card statements. Categorize your spending: groceries, dining, gas, travel, subscriptions, and general purchases. This gives you real numbers, not guesses.

- Identify your top two or three spending categories. These are where a rewards card will earn the most for you. A card offering 3% on dining is worth more to someone who spends $600 a month at restaurants than to someone who spends $60.

- Decide whether you carry a balance. For cardholders who carry balances, minimizing purchase APR outweighs rewards value. Interest costs generally erase any cashback or point benefits. If you pay in full every month, rewards become your primary metric.

- Match your credit tier to realistic card options. Spending pattern analysis is recommended before comparing cards to ensure rewards align with actual usage rather than marketing points.

Pro Tip: Project your annual card earnings by multiplying your monthly category spending by the reward rate, then multiply by 12. Compare that number across three or four cards to see which one actually pays you the most.

What are the most common pitfalls in credit card comparison?

Most mistakes in card comparison come from trusting marketing language over math. Here are the traps that catch people most often:

- Headline rewards without category limits. A card advertising 5% back sounds great until you realize the 5% only applies to one rotating category per quarter with a $1,500 spending cap. After the cap, you earn 1%.

- Ignoring the penalty APR. A single card has multiple APRs, and the penalty APR, triggered by a late payment, can exceed 29.99% on some cards. One missed payment can lock you into a much higher rate for months.

- Overlooking hidden fees. Foreign transaction fees, paper statement fees, and authorized user fees rarely appear in ads. They show up in the fine print and can add up to hundreds of dollars annually. Rate Grove’s guides flag these costs using verified issuer data so you do not have to hunt for them yourself.

- Applying without checking credit requirements. Many consumers overlook credit score tiers when comparing cards, leading to wasted applications and negative credit impacts.

- Comparing rewards without subtracting fees. A card earning $400 in annual rewards but charging a $450 annual fee is a net loss of $50. Always run the net benefit calculation before deciding.

“Calculating net benefits by subtracting fees from realistic projected rewards based on specific spending patterns yields the most accurate comparison. Relying on advertised rates alone produces a distorted picture of a card’s true value.”

Reading bank fee disclosures carefully applies the same discipline to credit cards. The skill transfers directly.

How can comparison tools simplify the selection process?

Digital comparison tools solve the biggest problem in card selection: the sheer volume of offers. Comparison tools improve accuracy by running real monthly spending data through earning rules including tiers, caps, and transfer partners, showing genuine rewards value side by side.

The best tools do more than list cards. They let you enter your actual spending by category and calculate projected annual rewards for each card on your list. That output is far more useful than any advertised rate.

| Feature | What it does for you |

|---|---|

| Spending input calculator | Projects real annual rewards based on your category spending |

| Fee breakdown display | Shows all fees, not just annual fees, for true cost comparison |

| Credit profile filter | Limits results to cards you are likely to be approved for |

| APR comparison | Displays purchase, transfer, and penalty APRs side by side |

| Net benefit calculation | Subtracts annual fees from projected rewards for a true value figure |

Rate Grove applies this approach directly. Its platform uses verified data from issuer and regulator sites to show side-by-side comparisons of fees, rates, and tradeoffs. The guides are updated monthly, so the numbers you see reflect current offers, not last year’s promotions.

Pro Tip: Use a comparison tool that lets you input your own spending amounts rather than relying on preset “average spender” profiles. The average profile rarely matches your actual habits, and the rewards projections will be off as a result.

Understanding introductory rate mechanics also helps when comparing cards that advertise 0% APR periods, since those offers have specific terms that affect their real value.

Key takeaways

Credit card comparison means evaluating fees, APRs, rewards, and credit requirements side by side, then filtering results through your own spending habits to find the card that delivers the highest net value for your situation.

| Point | Details |

|---|---|

| Definition of comparison | Credit card comparison is a structured, side-by-side evaluation of offers based on fees, rates, rewards, and credit fit. |

| Fees matter beyond the annual fee | Foreign transaction, late payment, and cash advance fees can cost hundreds annually and must be included in any comparison. |

| APR type depends on behavior | Carrying a balance makes purchase APR the most critical factor; rewards become secondary when interest costs are present. |

| Spending habits drive card fit | Projecting rewards from your actual category spending produces far more accurate comparisons than relying on advertised rates. |

| Net benefit is the real metric | Subtract annual fees from projected rewards to find the card’s true value before applying. |

Why I think most people compare credit cards the wrong way

By Mat C.

Most people start a credit card comparison by Googling “best rewards card” and clicking the first result. That approach hands the decision to whoever paid the most for a sponsored placement. It is not a comparison. It is a recommendation dressed up as one.

The honest starting point is your own bank statement. Spend 15 minutes categorizing three months of spending before you look at a single card offer. That exercise tells you more about which card fits your life than any top-ten list ever will. I have seen people sign up for premium travel cards while spending almost nothing on travel, simply because the card looked impressive. They paid $550 a year for benefits they never used.

The fine print deserves more attention than most people give it. Penalty APRs, spending caps on reward categories, and the difference between cash advance APR and purchase APR are not obscure details. They are the terms that determine whether a card costs you money or makes you money. Reading them takes 10 minutes and can save you years of unnecessary fees.

My practical advice: run the net benefit calculation before you apply to anything. Take your projected annual rewards, subtract the annual fee, and compare that number across three or four cards. The winner is rarely the card with the flashiest marketing. It is usually the card that matches your actual spending categories with the lowest total cost.

— Mat C.

Rate Grove makes credit card comparison straightforward

Finding the right credit card should not require hours of research across a dozen different websites.

Rate Grove’s credit card comparison platform pulls verified data directly from issuers and regulators, then presents fees, APRs, and rewards side by side in a format built for quick, clear decisions. You can filter by credit profile, spending category, and card type to focus only on offers that fit your situation. The guides are updated monthly, so you are always working with current numbers. Whether you are comparing your first card or evaluating an upgrade, Rate Grove gives you the full picture without the noise.

FAQ

What does credit card comparison mean?

Credit card comparison is the structured process of evaluating multiple credit card offers side by side based on fees, interest rates, rewards, and credit requirements to find the best fit for your financial habits.

What is the average credit card APR right now?

The average credit card APR as of may 2026 is 19.19%, according to Experian. Cards with lower rates typically require excellent credit to qualify.

How do I compare credit cards accurately?

Enter your actual monthly spending by category into a comparison tool, project annual rewards for each card, then subtract the annual fee to calculate the net benefit before applying.

Why does my credit score matter when comparing cards?

Applying to cards outside your credit tier triggers hard inquiries that lower your score and result in declined applications. Filtering comparisons to cards within your credit range improves both approval odds and the relevance of your results.

Are advertised rewards rates reliable for comparison?

Advertised rates are often the best-case scenario. Spending caps, category restrictions, and annual fees can significantly reduce real-world rewards value, so always calculate net benefit based on your own spending patterns.