Comparing student credit card rates is the single most effective way to avoid overpaying for credit while building a strong financial foundation. The industry term for this practice is “total cost of ownership” analysis, and it goes well beyond the advertised annual percentage rate (APR). Student cards vary widely in fees, approval requirements, rewards, and credit-reporting practices. Knowing why compare student card rates matters puts you in control before you ever fill out an application.

Why compare student card rates before applying

The benefits of student card comparison start with approval odds. A database of 1,500+ offers shows significant variance in approval requirements across student cards. That variance means the card you apply for first can determine whether you get approved at all, not just what rate you receive.

Many student cards are specifically designed for applicants with limited or no FICO credit history. Others require at least some established credit. Applying without comparing first risks a hard inquiry on your credit report and a rejection that makes the next application harder. Comparing before applying lets you match your actual credit profile to the right card.

Your income and enrollment status also affect the offers you qualify for. Some issuers require proof of enrollment at an accredited college. Others accept any young adult under a certain age. Knowing these filters in advance saves time and protects your credit score from unnecessary inquiries.

Pro Tip: Check whether a card explicitly states “no credit history required” before applying. Cards that advertise this feature are built for first-time credit users and carry the highest approval odds for students starting from zero.

Key factors that affect your approval odds and rate offer:

- Credit history length: No history typically means a higher APR offer.

- Income verification: Higher reported income can unlock better terms.

- Enrollment status: Some issuers require active college enrollment.

- Existing debt: Any current balances affect your debt-to-income ratio.

- Card-specific criteria: Each issuer sets its own minimum requirements.

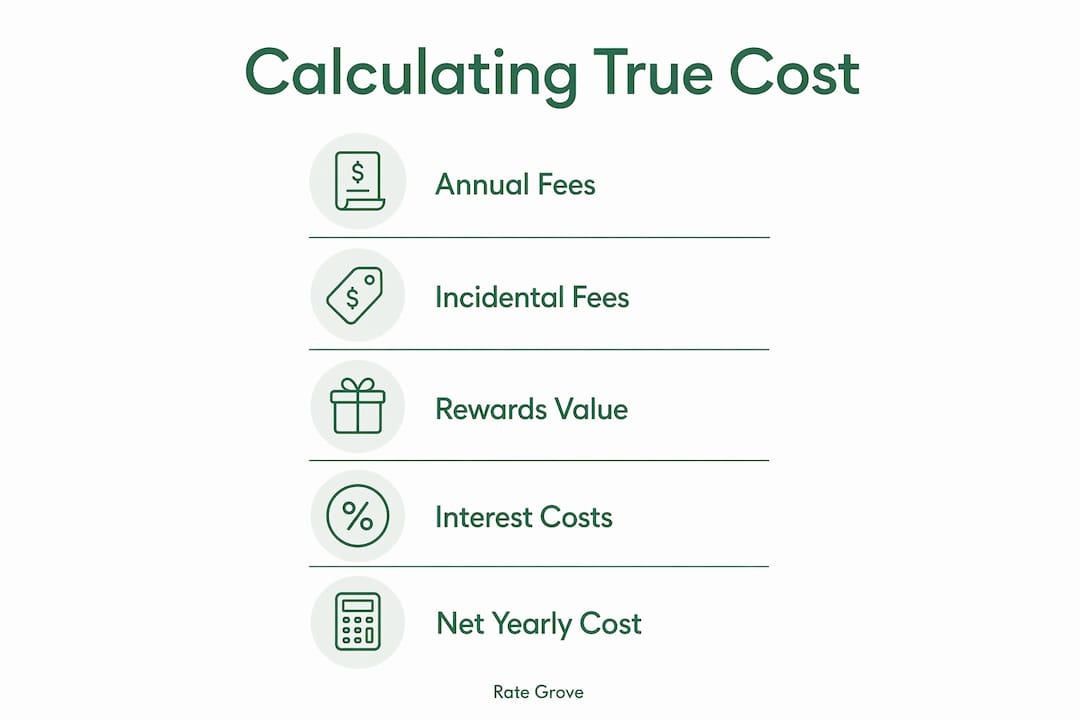

How to calculate the true cost of a student credit card

The advertised APR is only one piece of the cost picture. Total ownership costs include annual fees, incidental fees, foreign transaction fees, and the rewards you earn back. Looking at all four together gives you the real number.

The formula is straightforward: add up all annual fees, subtract the estimated annual rewards value, and factor in the interest cost if you expect to carry a balance. A card with a $39 annual fee and $60 in annual cash back rewards has a net benefit of $21 before interest. A no-fee card with no rewards is neutral. A card with a $0 fee but a 29% APR costs far more if you ever carry a balance.

| Cost Component | What to Look For | Example Impact |

|---|---|---|

| Annual fee | $0 to $39 range for student cards | Adds directly to yearly cost |

| Foreign transaction fee | Typically 3% per transaction | Significant for study abroad |

| Late payment fee | Up to $40 per occurrence | Avoidable with autopay |

| Cash back rewards | 1%–2% on purchases | Offsets fees when used consistently |

| Ongoing APR | 19%–29% range for student cards | Largest cost if you carry a balance |

A yearly cost-benefit analysis that subtracts rewards from fees is the industry best practice for identifying the true net cost. Most students skip this step and focus only on the sign-up bonus, which is a one-time benefit that disappears after the first year.

Pro Tip: Calculate your expected monthly spending in each rewards category before choosing a card. If you spend most of your money on groceries and gas, a flat 1.5% cash back card often outperforms a rotating category card that only rewards those categories one quarter per year.

Long-term APR is more valuable than a short introductory 0% offer for most students. A lower ongoing rate reduces your cost every month you carry a balance, while a 0% intro period ends and often resets to a high rate. Read the fine print on any introductory offer before treating it as a selling point. Understanding how introductory rates work helps you evaluate whether a promotional period actually benefits your spending habits.

Why credit bureau reporting is a critical comparison factor

Credit cards that report to all three major bureaus, Equifax, Experian, and TransUnion, build your credit history faster and more completely than cards that report to only one or two. This distinction rarely appears in marketing materials, but it is one of the most important features to compare.

Lenders who check your credit for a car loan or mortgage typically pull from all three bureaus. If your card only reports to one, two-thirds of your credit history may be invisible to those lenders. That gap can mean a higher rate on your next loan or a denial altogether.

Responsible card use during college, paying on time and keeping utilization low, builds the credit profile that supports major purchases after graduation. The card you choose now directly affects the interest rate you pay on a car loan in two years. That connection makes bureau reporting a financial decision, not just a technical detail.

Key reporting factors to verify before choosing a card:

- Reports to all three bureaus: Equifax, Experian, and TransUnion.

- Reports monthly: Some secured cards report less frequently.

- Reports the right data: Payment history and utilization, not just account existence.

- No reporting gaps: Confirm the issuer’s policy in writing if needed.

Many students mistakenly focus only on perks and miss whether a card reports to all bureaus or has manageable limits. Perks are nice. A complete credit history is worth thousands of dollars in lower borrowing costs over a lifetime.

Common misconceptions about student card features

The biggest misconception about student credit cards is that a higher credit limit is always better. Financial experts recommend lower limits for new credit users because they prevent excessive debt and keep utilization ratios manageable. A $500 limit forces discipline. A $3,000 limit on a student income creates real risk.

The second misconception is that rotating rewards categories are more valuable than flat-rate rewards. Flat-rate cash back consistently outperforms rotating categories for most students because it requires no tracking, no activation, and no missed quarters. Rotating categories reward specific spending types for 90-day periods. Students who forget to activate the category or who don’t spend in that category lose the benefit entirely.

| Feature | Common Belief | Reality |

|---|---|---|

| High credit limit | More flexibility | Higher debt risk for new users |

| Rotating rewards | More earning potential | Easy to miss; requires active management |

| 0% intro APR | Free money period | Resets to high rate; often misused |

| No annual fee | Always the best deal | May lack reporting or rewards that offset costs |

| Secured card | Only for bad credit | Legitimate starting point for zero-history students |

Comparing cards is the only reliable way to distinguish legitimate student cards from predatory credit-building products with excessive fees. Some cards marketed to students carry monthly maintenance fees, processing fees, and program fees that add up to hundreds of dollars per year. A side-by-side comparison exposes these costs immediately. Understanding how fees drain your savings applies equally to credit cards and bank accounts.

Students who use issuer-provided educational resources tend to have lower default rates and better credit outcomes. Cards that include budgeting tools, credit score monitoring, and spending alerts give you a built-in safety net. These features are worth comparing alongside rates and fees.

Key Takeaways

Comparing student credit card rates before applying is the most direct way to reduce costs, improve approval odds, and build a complete credit history from day one.

| Point | Details |

|---|---|

| Compare before applying | Matching your profile to card requirements protects your credit score from unnecessary hard inquiries. |

| Calculate total ownership cost | Subtract rewards from fees and factor in APR to find the real yearly cost of any card. |

| Verify bureau reporting | Cards that report to all three bureaus build credit history that lenders actually see. |

| Prioritize long-term APR | A lower ongoing rate saves more money than a short introductory 0% period. |

| Avoid predatory products | Side-by-side comparison is the only way to spot excessive fees before they cost you. |

What most students get wrong about card comparisons

I’ve watched students make the same mistake for years: they pick the card with the best sign-up bonus and stop there. The bonus is a one-time event. The APR, the fees, and the reporting practices follow you for years.

The detail I see overlooked most often is bureau reporting. A card that only reports to one bureau is essentially building a partial credit file. When that student applies for a car loan two years later, the lender pulls all three bureaus and sees a thin file. The student gets a higher rate or a denial. That outcome traces directly back to a comparison they skipped.

The second thing students miss is the difference between a card designed for them and a card designed to profit from them. Predatory products exist in this market. They use student-friendly language and target people with no credit history. The fees are buried in the fine print. A proper comparison, one that looks at the full fee schedule and not just the headline rate, catches these products before they do damage.

My honest advice: treat your first credit card like your first lease. Read every line. Compare at least three options. Look at what the card costs in year two, after any intro offer expires. The students who do this build credit efficiently and avoid the debt traps that follow others into their late twenties.

— Mat C.

Rate Grove makes student card comparison straightforward

Finding the best student card rates doesn’t require hours of research across a dozen websites. Rate Grove pulls verified data from issuer and regulator sites and presents fees, rates, and rewards side by side so you can see the full picture in one place.

Rate Grove updates its credit card comparison guides monthly, so the rates and terms you see reflect current offers, not outdated information. You can filter by fee structure, rewards type, and approval requirements to match cards to your actual profile. Whether you’re comparing your first card or looking to upgrade after a year of responsible use, Rate Grove gives you the verified data you need to choose with confidence.

FAQ

Why does comparing student card rates matter for approval?

Approval requirements vary significantly across student cards. Comparing cards before applying lets you target products that match your credit profile and avoid hard inquiries from likely rejections.

What is the most important factor beyond the interest rate?

Credit bureau reporting is the most overlooked factor. Cards that report to Equifax, Experian, and TransUnion build a complete credit history that lenders check when you apply for future loans.

Are lower credit limits actually better for students?

Financial experts recommend lower limits for new credit users because they reduce the risk of excessive debt and keep utilization ratios manageable, both of which support a stronger credit score.

How do I find the true yearly cost of a student card?

Add the annual fee, estimate any incidental fees, then subtract your expected annual rewards. Factor in interest costs if you plan to carry a balance. That total is your real yearly cost.

Is flat-rate cash back better than rotating rewards for students?

Flat-rate rewards are more reliable for most students. Rotating category bonuses require activation and specific spending patterns that many students miss, resulting in lower actual earnings.