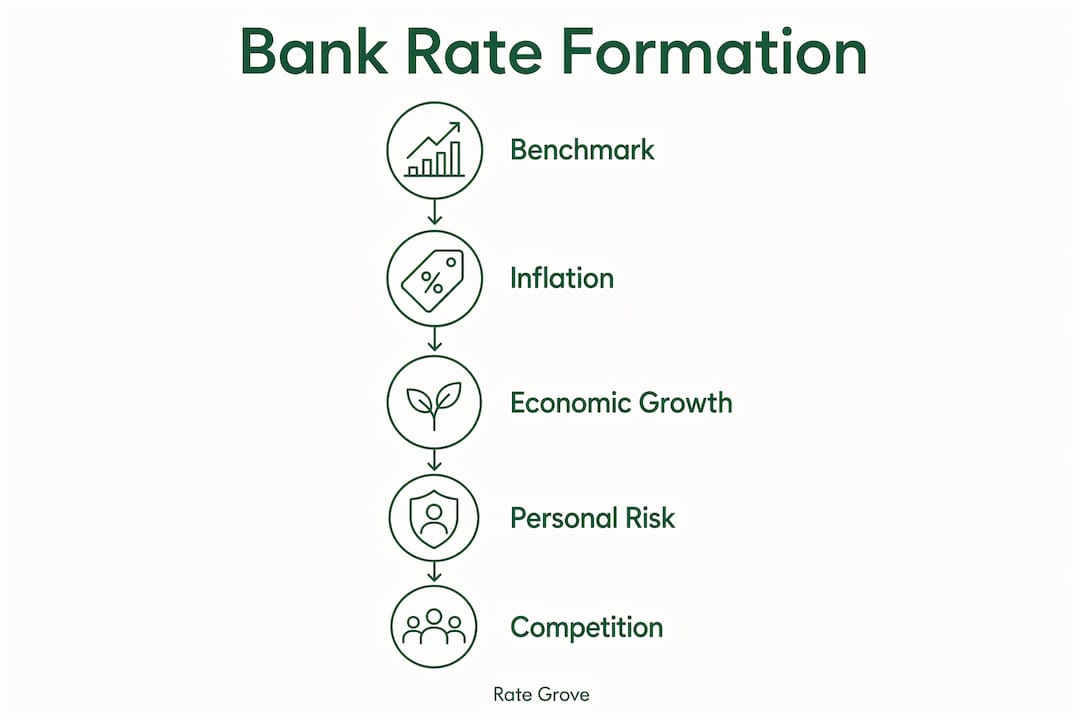

Bank rates are determined by a combination of the federal funds rate, inflation expectations, and individual borrower risk. Understanding how bank rates are set tells you why your savings account earns what it does, why your mortgage costs what it costs, and when the best time to borrow or save actually is. The Federal Reserve sets the foundational benchmark, but inflation, credit scores, and bank competition all shape the final number you see. This guide breaks down each layer so you can read rate changes with confidence.

How bank rates are set: the federal funds rate as the foundation

The federal funds rate is the overnight rate at which banks lend money to each other. The Federal Reserve sets a target for this rate at its Federal Open Market Committee meetings, which happen roughly eight times per year. Every retail bank in the country watches this number closely because it sets the floor for what borrowing money costs.

Banks use the federal funds rate as a benchmark to price both their deposit products and their loans. When the Fed raises the rate, banks typically raise their loan rates quickly and their deposit rates more slowly. That gap between what banks pay depositors and what they charge borrowers is called the Net Interest Margin, or NIM. Managing NIM is the central task of bank rate setting.

The yield curve also shapes how banks price products. A normal yield curve slopes upward, meaning long-term rates are higher than short-term rates. Banks borrow short (from depositors) and lend long (mortgages, auto loans), so a steep yield curve widens their profit margin. A flat or inverted yield curve compresses that margin and often signals tighter credit conditions ahead.

Key monetary policy tools the Federal Reserve uses to influence the federal funds rate include:

- Open market operations: Buying or selling Treasury securities to add or remove money from the banking system

- The discount rate: The rate the Fed charges banks for direct loans, which sets an upper boundary on overnight borrowing costs

- Reserve requirements: The share of deposits banks must hold, which affects how much they can lend

- Forward guidance: Public statements about future rate intentions, which shape market expectations before any actual rate change

Pro Tip: Watch the Federal Reserve’s post-meeting statements, not just the rate decision itself. The language around future moves often signals where your savings and loan rates are heading over the next six months.

How do inflation and GDP growth affect bank interest rates?

Inflation acts as a mandatory premium that banks build into every rate they offer. If a bank lends you money at 4% but inflation runs at 3%, the bank’s real return is only 1%. Banks price this risk in from the start, which is why rising inflation almost always produces rising loan rates.

Central banks set explicit inflation targets to anchor expectations. The Bank of England, for example, targets 2% annual inflation. When inflation climbs above that target, the central bank raises its benchmark rate to cool spending. That rate increase flows directly into the rates your bank charges on credit cards, mortgages, and personal loans.

GDP growth also matters. Strong economic growth increases demand for loans, which gives banks room to charge more. Slow growth or recession reduces loan demand, which pushes banks to compete harder on rate to attract borrowers. The table below shows how these two variables typically move bank rates:

| Economic condition | Inflation trend | Typical bank rate direction |

|---|---|---|

| Strong GDP growth | Rising | Rates increase |

| Moderate GDP growth | Stable near target | Rates hold steady |

| Slow GDP growth | Falling | Rates decrease |

| Recession | Below target | Rates fall sharply |

Structural economic shifts also shape long-term rate trends. Demographic aging and rising demand for safe assets have pushed real interest rates downward over decades. This is why the baseline rate environment of the 2010s was so much lower than the 1980s, even after adjusting for inflation.

Pro Tip: Track the Consumer Price Index (CPI) monthly. When CPI rises faster than the Fed’s 2% target for two or more consecutive months, a rate hike is likely within the next quarter. That’s your signal to lock in a fixed-rate loan or a CD before rates climb further.

What personal factors do banks use to set your individual rate?

Your personal credit profile determines how much above the benchmark rate you actually pay. Credit score and debt-to-income ratio are the two most influential borrower-specific variables. A higher debt-to-income ratio signals that you are already stretched thin, which raises the bank’s risk and your rate.

Banks call this approach risk-based pricing. The riskier you look on paper, the higher the rate the bank charges to compensate for the chance you might not repay. This is not arbitrary. Banks use statistical models built on millions of loan outcomes to predict default probability and price it into your offer.

Credit history length and payment timeliness also carry significant weight. A borrower with ten years of on-time payments looks very different to a bank than someone with three years of mixed history, even if their current scores are similar. Longer, consistent credit history generally earns a lower rate.

Banks also evaluate these factors when pricing a specific loan:

- Loan type: Secured loans (backed by collateral like a home or car) carry lower rates than unsecured personal loans because the bank can recover losses if you default.

- Down payment size: A larger down payment reduces the bank’s exposure, which typically lowers your mortgage rate.

- Loan term: Shorter loan terms usually carry lower rates because the bank’s money is at risk for less time.

- Collateral quality: The type and value of collateral affects the rate. A new car depreciates faster than a home, so auto loan rates often reflect that higher risk.

- Loan purpose: Some lenders price home improvement loans differently than debt consolidation loans because the underlying risk profiles differ.

Competition between banks also shapes what you are offered. If three banks are competing for your mortgage, each will sharpen its rate to win your business. Knowing this gives you real negotiating power. You can read more about how bank fees affect your savings alongside rate differences to get the full picture of what an account actually costs you.

How do banks balance profitability, competition, and regulation?

Pricing interest rates is a balancing act between profitability, customer appeal, competitive positioning, and regulatory compliance. Banks cannot simply set whatever rate maximizes short-term profit. They operate within regulatory frameworks that limit certain practices and require transparent disclosure.

Non-performing assets force banks to raise rates on healthy borrowers to cover losses from defaults. When a significant share of a bank’s loan book goes bad, the cost of those losses gets spread across the performing portfolio. This is one reason why rates at banks with weaker loan quality can run higher than those at well-managed institutions.

Banks also use demand forecasting and price elasticity analysis to time rate changes. Some products are highly elastic, meaning customers switch providers quickly when rates change. Savings accounts and CDs fall into this category. Banks respond with layered pricing tactics, such as introductory rates, relationship bonuses, and tiered rate structures, to retain customers without permanently committing to a high rate. You can learn more about how introductory rates work and why banks use them as a competitive tool.

“Interest rates act as a primary tool for controlling economic activity. Raising rates cools demand by increasing borrowing costs, while lowering rates encourages spending.” — Bank of England

Regulatory compliance adds another layer. Capital adequacy rules, consumer protection laws, and stress-testing requirements all constrain how aggressively a bank can price its products. A bank that appears to offer a great rate may be doing so because it is taking on more risk elsewhere in its portfolio.

Key Takeaways

Bank rates reflect a layered system where the federal funds rate sets the floor, inflation and economic conditions shape the range, and your personal credit profile determines your exact offer.

| Point | Details |

|---|---|

| Federal funds rate is the foundation | The Federal Reserve’s benchmark rate sets the starting point for all retail bank loan and deposit pricing. |

| Inflation drives mandatory rate premiums | Banks add an inflation buffer to every rate to protect the real value of money lent or invested. |

| Credit score shapes your personal rate | Higher credit scores and lower debt-to-income ratios consistently produce lower offered rates. |

| NIM management drives bank strategy | Banks profit from the spread between short-term deposit rates and long-term loan rates. |

| Competition and regulation constrain pricing | Banks balance rate competitiveness against regulatory requirements and portfolio risk. |

Why understanding rate mechanics changes how you borrow and save

Most people treat bank rates as fixed facts, like the weather. You check the number, accept it, and move on. That approach costs real money over time.

What I have found after years of watching rate cycles is that timing matters more than most borrowers realize. The window between a Federal Reserve rate decision and the moment banks fully pass that change to depositors is often several weeks. Savers who move quickly into high-yield savings accounts or CDs right after a Fed hike capture rates that latecomers miss entirely. The same logic applies in reverse when rates fall: locking in a fixed-rate CD before cuts arrive protects your yield for months.

The credit score piece is where I see the most preventable losses. A borrower with a 680 credit score and a 720 score can receive meaningfully different mortgage rates from the same bank on the same day. That difference compounds over a 30-year loan into tens of thousands of dollars. Spending six months paying down revolving debt before applying for a major loan is one of the highest-return financial moves available to most people.

The non-performing asset issue is one most consumers never hear about. If your bank has been aggressive in a particular lending category and defaults are rising, you may be quietly subsidizing those losses through slightly higher rates on your own products. Checking a bank’s financial health before committing to a long-term CD or savings relationship is worth the ten minutes it takes.

— Mat C.

Find rates that actually reflect the current market

Knowing how interest rates are determined is only useful if you can see what banks are actually offering right now. Rate changes move fast, and the gap between the best and worst offers in any category can be significant.

Rate Grove compares current rates on CDs, bank accounts, and credit cards side by side, using verified data pulled directly from issuer and regulator sources. Every comparison includes fees and tradeoffs, not just the headline rate. If you want to see which accounts are paying the most given today’s rate environment, compare current rates at Rate Grove and get a clear, current picture in minutes.

FAQ

What is the federal funds rate and why does it matter?

The federal funds rate is the overnight rate banks charge each other for short-term loans. It serves as the primary benchmark for all retail bank lending and deposit rates in the United States.

How does inflation affect the interest rate on my loan?

Inflation forces banks to add a premium to loan rates to preserve the real value of money they lend. When inflation rises above central bank targets, benchmark rates increase, and your loan rate follows.

Can I negotiate a lower interest rate with my bank?

Yes. Banks compete for creditworthy borrowers, and presenting competing offers often produces a better rate. Improving your credit score and reducing your debt-to-income ratio before applying gives you the strongest negotiating position.

Why do two people get different rates from the same bank?

Banks use risk-based pricing, meaning your credit score, debt-to-income ratio, loan type, and collateral all produce a unique rate offer. Two borrowers applying the same day can receive rates that differ by a full percentage point or more.

How often do bank rates change?

Banks can adjust rates at any time, but the most common triggers are Federal Reserve rate decisions, significant shifts in inflation data, and competitive pressure from other lenders. Savings and CD rates often move within days of a Fed announcement.