Your credit score is the single most influential number in any credit application, shaping whether you get approved, what interest rate you pay, and how much a single application costs your score. The credit score impact on credit applications begins the moment a lender pulls your report, triggering a hard inquiry that can lower your FICO score by a small but real amount. Understanding how this works gives you the power to apply at the right time, for the right products, with the best possible odds. This guide covers the mechanics, the thresholds, the timing rules, and the preparation steps that matter most in 2026.

What happens to your credit score when you apply for credit

Every credit application triggers a hard inquiry, and that inquiry directly affects your score. A single hard inquiry typically lowers a FICO score by 5 points or less for consumers with established credit profiles. That is a small drop, but it compounds quickly when you apply for multiple products in a short window.

The key distinction is between hard and soft inquiries. A hard inquiry happens when a lender reviews your full credit report to make a lending decision. A soft inquiry happens when you check your own score, or when a lender pre-screens you for an offer. Soft inquiries do not affect your score at all.

Hard inquiries stay on your credit report for two years, but they only affect your score for the first 12 months. That distinction matters. Many people assume a hard inquiry haunts their score for the full two years. It does not. The visible record stays, but the scoring penalty disappears after 12 months.

Here is what the inquiry process looks like in practice:

- Hard inquiry: Triggered by a formal credit application (credit card, personal loan, mortgage, auto loan). Lowers your score temporarily.

- Soft inquiry: Triggered by prequalification checks, employer background checks, or your own credit monitoring. Zero score impact.

- Multiple hard inquiries: Each one adds a small penalty. Lenders also read a cluster of recent inquiries as a sign of financial stress, which can hurt your approval odds beyond the score drop itself.

- Denied applications: A denial does not add any extra penalty beyond the hard inquiry already recorded. The score drop is the same whether you are approved or rejected.

Pro Tip: Before applying for any credit product, ask the lender whether they use a hard or soft pull for prequalification. Many lenders now offer soft-pull prequalification, which lets you see your approval odds without touching your score.

One detail most people miss: FICO scoring requires at least one account open for six months and one account reported within the last six months to generate a score. New credit users who open their first account may not see score improvements right away, even after responsible use begins.

How do credit score thresholds affect loan approval and rates?

Credit score thresholds are the cutoff points lenders use to decide who qualifies and at what price. A minimum score of 580 is typically required to qualify for a personal loan, while scores in the 700s unlock the most competitive interest rates. That gap between qualifying and getting a good rate is where most people lose money.

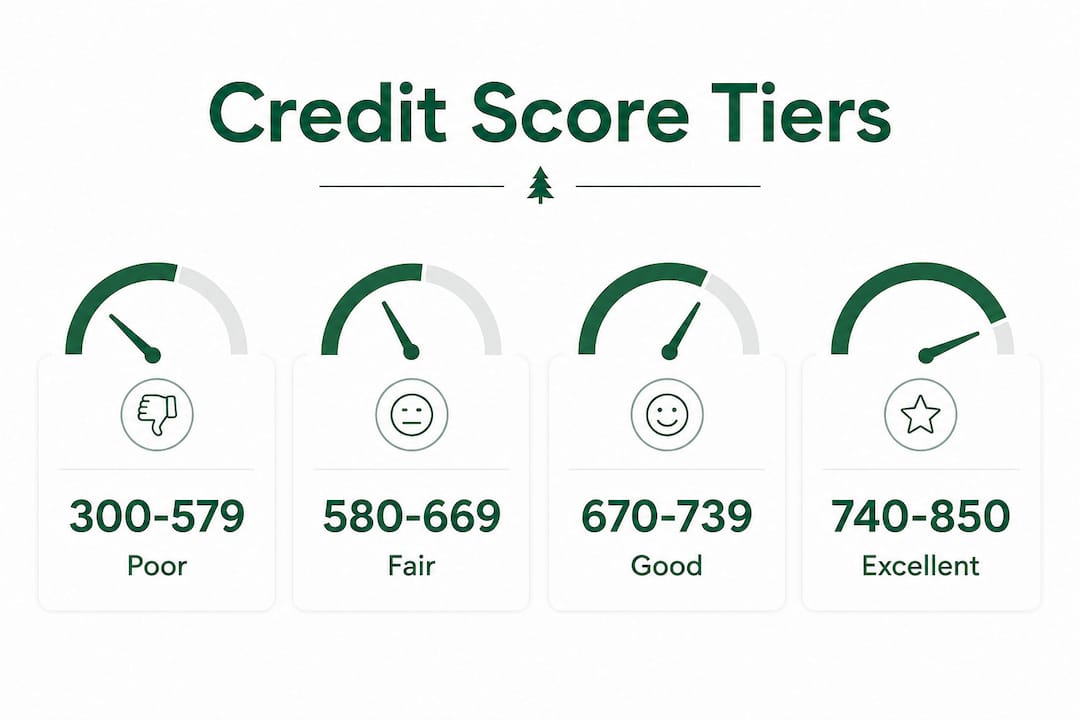

A FICO score of 670 or higher is classified as “good,” while scores of 740 and above reach “very good” or “excellent” territory. Lenders use these benchmarks to set approval likelihood and pricing tiers. The difference between a 620 score and a 740 score on a mortgage can mean thousands of dollars in extra interest over the life of the loan.

| Credit score range | Classification | Typical lender response |

|---|---|---|

| 300–579 | Poor | Most applications denied; secured cards only |

| 580–669 | Fair | Limited approvals; higher rates and fees |

| 670–739 | Good | Broad approval access; competitive rates |

| 740–799 | Very good | Strong approval odds; near-best rates |

| 800–850 | Exceptional | Best rates and terms available |

Lenders price risk directly into interest rates. A lower score signals a higher chance of default, so the lender charges more to offset that risk. This is called risk-based pricing, and it affects every credit product from credit cards to auto loans to mortgages.

Your score is not the only factor lenders weigh. Payment history, credit utilization, length of credit history, and credit mix all feed into the FICO model. Credit mix accounts for about 10% of your FICO score. Adding a new credit card can improve this factor over time, which is one reason a well-timed application can actually help your profile in the long run.

Pro Tip: Check the credit score requirements for a specific product before applying. Many lenders publish their minimum score requirements publicly, or you can find them through a credit card comparison resource. Applying within your range protects your score from unnecessary hard inquiries.

How does timing affect the impact of credit inquiries?

Timing is the most underrated factor in managing how credit applications affect your score. Experts recommend waiting at least six months between credit card applications to prevent compounding negative effects. Each inquiry adds a small penalty, and a cluster of inquiries in a short period signals financial distress to lenders.

Multiple recent hard inquiries do more than lower your score by a few points each. Lenders view a pattern of recent inquiries as a sign that you are in financial trouble or taking on more debt than you can handle. That perception can trigger a denial even when your score technically meets the minimum threshold.

There is one important exception to the multiple-inquiry rule. When you shop for a mortgage or auto loan, credit bureaus and FICO treat multiple inquiries for the same loan type within a short window (typically 14 to 45 days) as a single inquiry. Rate shopping for a home loan does not hurt your score the same way applying for five credit cards does.

Here are the best practices for timing your credit applications:

- Wait six months between credit card applications. This gives your score time to recover and shows lenders a stable pattern.

- Use prequalification tools first. Soft inquiry prequalification lets you gauge your approval odds without any score impact.

- Cluster mortgage or auto loan rate shopping. Do all your rate comparisons within a 14 to 45 day window to count as one inquiry.

- Avoid applying for new credit in the months before a major loan. A mortgage lender will see every recent inquiry and may question your financial stability.

- Track your inquiry count. Pull your free credit report and count active hard inquiries before submitting any new application.

Pro Tip: If you are planning a major purchase like a home or car within the next six months, freeze all other credit applications. One extra credit card inquiry at the wrong time can shift your rate tier and cost you real money.

Steps to prepare before applying for credit

Preparation before a credit application reduces score damage and raises your approval odds. The goal is to walk into an application with the strongest possible profile, not to fix problems after a denial.

- Check your credit report for errors. Request your free report from AnnualCreditReport.com and look for accounts you do not recognize, incorrect balances, or late payments that were actually on time. Errors are more common than most people expect, and disputing them is free.

- Lower your credit utilization. Keeping utilization below 30% supports higher scores; below 10% is even better. Pay down balances before applying, not after.

- Know your score before the lender does. Use a free credit monitoring service or your bank’s score tool to see where you stand. Applying blind is the most avoidable mistake in credit management.

- Use prequalification to filter your options. Many credit card issuers and personal loan lenders offer soft-pull prequalification. Use it to narrow your choices before committing to a hard inquiry.

- Match the product to your profile. Applying for a premium rewards card when your score is 620 wastes a hard inquiry and a denial. Look at credit card APR factors to find products built for your score range.

- Space your applications around major loan plans. If a mortgage is on the horizon, hold off on any new credit applications for at least six months beforehand.

The preparation process is not complicated. It is mostly about knowing your numbers, fixing what you can fix quickly, and applying only when the timing and product fit are right.

Key Takeaways

Your credit score directly controls your approval odds, interest rates, and the short-term cost to your score every time you apply for credit.

| Point | Details |

|---|---|

| Hard inquiries cause a small drop | A single hard inquiry lowers your FICO score by 5 points or less and recovers within 12 months. |

| Score thresholds determine your terms | A score of 580 qualifies for most personal loans; 700+ unlocks the best interest rates. |

| Timing protects your score | Wait at least six months between credit card applications to avoid compounding score damage. |

| Prequalification is risk-free | Soft-pull prequalification tools let you check approval odds without affecting your score. |

| Preparation raises approval odds | Lowering utilization, fixing report errors, and matching products to your score range all improve outcomes. |

What I have learned from years of watching people apply for credit

Most people treat a credit application like a lottery ticket. They apply for whatever looks good, cross their fingers, and then wonder why their score dropped or why they got a worse rate than expected. The mechanics are not mysterious. They are just ignored.

The insight that changed how I think about this: the score drop from a single hard inquiry is almost never the real problem. The real problem is applying for the wrong product at the wrong time, collecting a denial, and then applying again somewhere else. That chain of events does far more damage than one well-timed application ever would.

Consumers consistently overestimate how long a hard inquiry hurts them. The score impact fades after 12 months even though the inquiry stays visible for two years. That fear of the two-year mark keeps people from applying when they should, and it keeps them from understanding that a good payment history after approval rebuilds a score faster than almost anything else.

My honest advice: stop chasing a perfect score and start building a clean record. Pay on time, keep balances low, and apply only when you have a specific need and a reasonable chance of approval. The score follows the behavior. It always does.

— Mat C.

Rate Grove makes credit comparison clearer

Choosing the right credit product before you apply is the single best way to protect your score and get better terms. Rate Grove compares credit cards, bank accounts, and CD rates side by side, using verified data from issuers and regulators so you are never working from outdated information.

Rate Grove is built for people who want clear answers fast. Every comparison shows fees, rates, and tradeoffs in plain language, so you can find the product that fits your credit profile without burning a hard inquiry on a long shot. Visit Rate Grove to compare your options and apply with confidence.

FAQ

How much does a credit application lower your score?

A single hard inquiry from a credit application typically lowers your FICO score by 5 points or less. The impact recovers within a few months for most consumers with established credit histories.

How long does a hard inquiry affect your credit score?

Hard inquiries remain on your credit report for two years but only affect your score for the first 12 months. After 12 months, the scoring penalty disappears even though the inquiry stays visible.

What credit score do you need to get a personal loan?

Most lenders require a minimum score of 580 to qualify for a personal loan. Scores in the 700s typically qualify for the most competitive interest rates and terms.

Does getting denied for credit hurt your score more?

No. A denial does not add any extra penalty beyond the hard inquiry already recorded. The score impact is the same whether your application is approved or rejected.

Can you check your approval odds without hurting your score?

Yes. Prequalification tools use soft inquiries that have no effect on your credit score. Use them to filter your options before committing to a formal application and a hard inquiry.