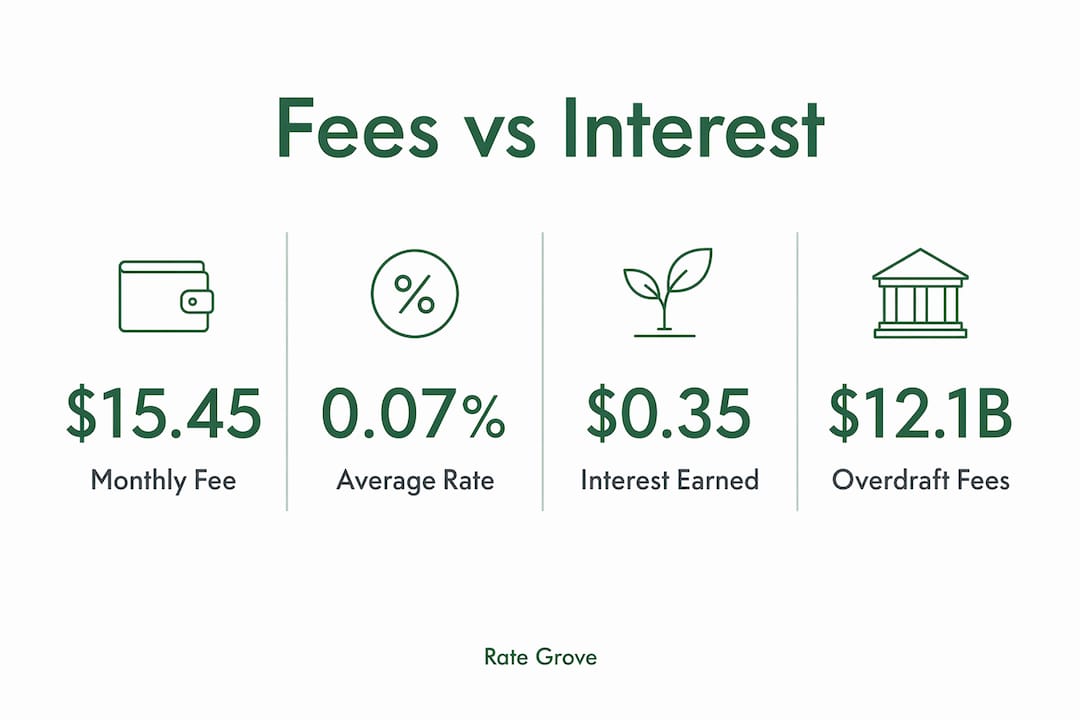

Comparing checking account rates and fees is the single most effective way to stop losing money to costs you never agreed to pay. The average monthly maintenance fee on a non-interest checking account hit $15.45 as of may 2026, which adds up to more than $185 a year if you never meet the waiver conditions. Meanwhile, the average interest rate on a checking account sits at just 0.07%. That gap tells you everything: fees cost far more than interest earns. Knowing why you should compare checking account rates is the first step toward choosing an account that actually works for your money.

Why compare checking account fees and rates?

The core reason to compare checking account rates is simple: fees almost always outpace interest earnings, especially on everyday balances. A checking account paying 0.07% on a $2,000 balance earns roughly $1.40 a year. One monthly maintenance fee wipes that out in a single billing cycle. The math is not close.

Banks count on customer inertia to keep fee revenue steady. Most people stay in high-fee accounts for years simply because switching feels like a hassle. That inertia costs real money every month.

A bank account fee comparison in 2026 also reveals how wide the gap between institutions has grown. Online banks and credit unions now routinely offer free checking with no minimum balance requirements. Large traditional banks still charge $10 or more per month as a baseline. Choosing without comparing means you may be paying for a service you could get free elsewhere.

What are checking account fees and why do they matter?

Checking account fees are charges your bank deducts directly from your balance. They reduce your money without any action on your part. Understanding each fee type is the foundation of any smart bank account fee comparison.

The most common fees you will encounter include:

- Monthly maintenance fees: The national average is $15.45 per month. Banks typically waive this fee if you maintain a minimum daily balance (often $1,500 or more) or set up a qualifying direct deposit.

- Overdraft fees: Americans paid $12.1 billion in overdraft and NSF fees in 2024. The average overdraft fee runs $26.77 per occurrence. A single forgotten subscription charge can trigger this.

- Non-sufficient funds (NSF) fees: These apply when a transaction is declined due to low funds. The fee amount is similar to overdraft fees and can stack up fast.

- Out-of-network ATM fees: Your bank charges one fee, the ATM operator charges another. Combined, these can reach $5 or more per withdrawal.

- Paper statement fees: Some banks charge $1 to $3 per month if you receive a mailed statement instead of going paperless.

The overdraft figure deserves a closer look. $12.1 billion paid in a single year means millions of Americans are absorbing a fee that many banks have reduced or eliminated entirely. Knowing which banks have dropped or capped overdraft fees is a direct benefit of comparing accounts before you open one.

Pro Tip: Read the fee disclosure table in any account agreement before signing. Banks are required to publish this document, and it lists every fee in plain language. Rate Grove’s guide to reading fee disclosures walks you through exactly what to look for.

How do interest rates on checking accounts affect your money?

The average checking account interest rate is 0.07% as of may 2026. That number reflects a fundamental truth about checking accounts: they are built for access and convenience, not wealth growth. Chasing interest in a checking account is the wrong priority for most people.

The table below shows how interest earnings compare to a single monthly maintenance fee at the 0.07% rate across different balance levels.

| Balance | Annual interest at 0.07% | One monthly maintenance fee |

|---|---|---|

| $500 | $0.35 | $15.45 |

| $1,000 | $0.70 | $15.45 |

| $2,000 | $1.40 | $15.45 |

| $5,000 | $3.50 | $15.45 |

The pattern is clear at every balance level. Even at $5,000, interest earnings do not cover one month of maintenance fees. This is why fee avoidance matters far more than rate chasing when you compare bank accounts.

Nearly 90% of interest-paying checking accounts carry monthly maintenance fees, often with high minimum balance requirements to waive them. So the accounts that pay the most interest frequently cost the most to hold. The net benefit shrinks fast.

Pro Tip: If you want your money to earn real interest, move excess funds to a high-yield savings account or a CD. Rate Grove’s guide on high-yield checking accounts explains when a higher-rate checking account actually makes sense.

What else should you evaluate when comparing checking accounts?

Fees and interest rates are the starting point, but the best checking account for you depends on how you actually use your money day to day. No single bank fits every person’s habits and needs.

Branch access vs. online banking

Traditional banks offer physical branches for cash deposits, notary services, and in-person support. Online banks skip the branches and pass the savings to you through lower fees and better rates. If you deposit cash regularly, an online-only account creates friction. If you rarely visit a branch, you may be paying for a service you never use.

ATM network size and fee reimbursement

A large ATM network means fewer out-of-network fees. Some online banks reimburse ATM fees up to a set monthly limit, which effectively gives you nationwide access for free. Check both the network size and the reimbursement cap before deciding.

Features that affect daily banking

- Mobile app quality: Look for mobile check deposit, real-time transaction alerts, and easy fund transfers. A poor app turns routine tasks into frustrations.

- Overdraft protection options: Some banks link your checking to a savings account for free overdraft coverage. Others charge a transfer fee. A few have eliminated overdraft fees entirely.

- Customer service availability: 24/7 phone or chat support matters when something goes wrong on a weekend.

- Transaction limits: Some accounts cap the number of free transactions per month. High-volume users should confirm there are no per-transaction charges.

A hybrid banking strategy pairs a free local checking account for everyday deposits and withdrawals with an online high-yield savings account for interest earnings. This approach gives you the physical access of a traditional bank and the better returns of an online institution. Rate Grove’s guide on moving from checking to savings covers how to set this up without disrupting your cash flow.

How to compare checking account fees and rates effectively

A structured approach saves time and prevents costly oversights. Use these steps to run a bank account fee comparison that actually leads to a better account.

- List your current fees. Pull three months of bank statements and total every fee charged. Monthly maintenance, overdraft, and ATM fees are the most common culprits. This number becomes your baseline.

- Read the fee disclosure document. Every bank publishes a schedule of fees. Focus on the monthly maintenance fee, the waiver conditions, the overdraft fee, and the ATM policy. Rate Grove’s guide on small balance fee drain shows how these fees hit smaller balances hardest.

- Check waiver conditions honestly. A $15 monthly fee waived by a $1,500 minimum balance is only free if you consistently hold that balance. If your balance dips below the threshold regularly, the fee applies. Be realistic about your typical balance.

- Compare at least three accounts. Look at one traditional bank, one online bank, and one credit union. Online banks and credit unions are the most likely sources of truly free checking in 2026.

- Plan your account switch carefully. Opening a new checking account triggers only a soft credit inquiry, so your credit score is not affected. However, migrating direct deposits and autopay requires a 2 to 4 week overlap period to prevent missed payments.

- Review your account annually. Fee structures change. A free account today may add fees next year. Set a calendar reminder each january to run a quick comparison.

Pro Tip: Set up direct deposit at your new account before closing the old one. Most employers process direct deposit changes within one to two pay cycles. Running both accounts in parallel during that window prevents any gap in access to your paycheck.

Key Takeaways

Avoiding fees matters more than earning interest on a checking account, because fees at $15.45 per month far outpace the 0.07% average interest rate at any typical balance.

| Point | Details |

|---|---|

| Fees exceed interest earnings | A $15.45 monthly fee costs more annually than 0.07% interest earns on most balances. |

| Overdraft fees add up fast | Americans paid $12.1 billion in overdraft and NSF fees in 2024, averaging $26.77 per occurrence. |

| Free checking still exists | Online banks and credit unions offer accounts with no monthly fees or minimum balance requirements. |

| Hybrid strategy works best | Pair a free local checking account with an online high-yield savings account for both access and returns. |

| Switch carefully | Allow a 2 to 4 week overlap when migrating direct deposits to avoid missed payments. |

The fee trap most people never see coming

I have spent years reviewing bank accounts, and the pattern I see most often is not reckless spending. It is quiet, automatic fee erosion. Someone opens a checking account in their twenties, sets up direct deposit, and never looks at it again. A decade later, they have paid thousands of dollars in fees they could have avoided entirely.

The checking account rate differences between institutions are real, but the interest gap is almost never the story worth telling. The fee gap is. A traditional bank charging $15.45 a month versus a credit union charging nothing is a $185 annual difference with zero benefit to the account holder. That money does not buy better service or better protection. It just disappears.

What I find most useful is the annual review habit. Once a year, pull your fee total for the past 12 months and compare it against what a free account would have cost you. That single number, seen clearly, motivates action faster than any financial advice. Most people are genuinely surprised by what they find.

The hybrid approach, free local checking plus online savings, is the most practical setup for most people I have seen. It is not complicated. It just requires one deliberate decision instead of the default of staying put.

— Mat C.

Rate Grove makes checking account comparison straightforward

Finding the right checking account means cutting through fee schedules, rate tables, and waiver conditions that vary by institution. Rate Grove pulls verified data from issuer and regulator sources so you can see fees, rates, and tradeoffs side by side without digging through multiple bank websites.

Rate Grove updates its guides monthly, so the numbers you see reflect 2026 conditions, not data from two years ago. Whether you are comparing maintenance fees, evaluating overdraft policies, or deciding between a traditional and online bank, the Rate Grove comparison tool gives you a clear starting point. Spend five minutes comparing now and you could save more than $185 this year.

FAQ

What is the average checking account fee in 2026?

The average monthly maintenance fee for a non-interest checking account is $15.45 as of may 2026, totaling more than $185 annually if waiver conditions are not met.

Does comparing checking accounts hurt my credit score?

Opening a new checking account triggers only a soft credit inquiry, which does not affect your credit score. The main risk is timing: migrating direct deposits and autopay requires a 2 to 4 week overlap to avoid missed payments.

Why do checking account fees matter more than interest rates?

The average checking account interest rate is 0.07%, which earns less than $4 a year on a $5,000 balance. A single monthly maintenance fee at the national average costs more than $15. Avoiding fees delivers a far greater financial benefit than earning interest.

What types of checking accounts have no monthly fees?

Online banks and credit unions are the most reliable sources of free checking in 2026. They typically require no minimum balance and charge no monthly maintenance fee, unlike most large traditional banks.

How often should I compare my checking account?

Review your checking account fees and features at least once a year. Fee structures change, and a free account today may introduce fees in a future terms update. An annual review takes less than 30 minutes and can identify savings opportunities immediately.