A savings strategy is defined as a deliberate plan to move money from a spending account into interest-bearing accounts on a consistent schedule. Most people keep too much cash in checking, where it earns nothing, while a structured approach to transfer funds from checking can generate meaningful interest over time. Financial experts recommend saving 5%–20% of take-home pay as a baseline, and building an emergency fund covering 3–6 months of essential expenses. Getting this right means choosing the correct account type, automating transfers, and knowing which fees to avoid before they quietly eat your progress.

What do you need before you move from checking to savings strategy?

Before you transfer a single dollar, you need a clear picture of your monthly cash flow. Add up every income source and every fixed expense. What remains is your “savings margin,” and that number determines how much you can realistically move each month without triggering overdrafts.

Choosing the right account type is the next decision. Three options cover most situations:

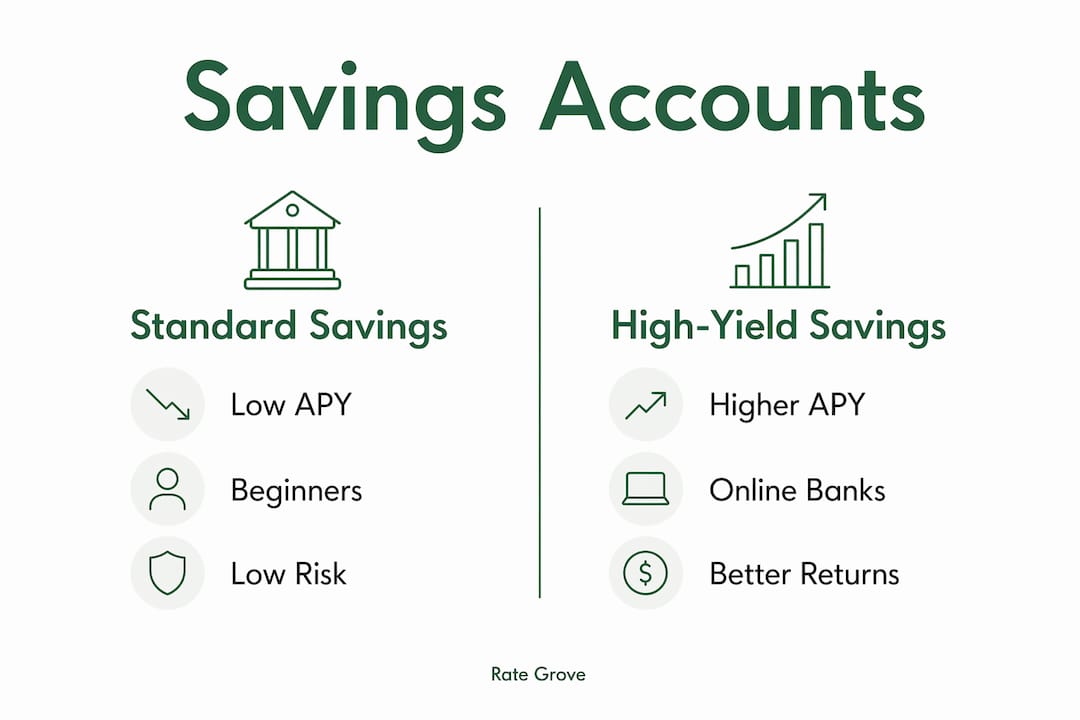

- Standard savings account: Low or no fees, but typically low interest rates. Good for beginners who want simplicity.

- High-yield savings account (HYSA): Offered mainly by online banks, these accounts pay significantly more than traditional savings. Online banks pay more because they carry lower overhead costs.

- Money market account: Often includes check-writing or debit access, with rates between standard and high-yield accounts. Best for savers who want some liquidity alongside better interest.

Transfer timing also matters before you set anything up. Internal transfers process instantly when both accounts are at the same bank. External transfers between different institutions take 1–3 business days. That delay affects when funds are available, so factor it into your bill payment schedule.

| Account type | Typical APY range | Best for |

|---|---|---|

| Standard savings | Very low (near 0.38%) | Beginners, simplicity seekers |

| High-yield savings | Significantly above average | Maximizing interest earnings |

| Money market | Moderate to high | Savers needing some access |

Pro Tip: Open your savings account at a different bank than your checking account. The extra step required to move money back creates friction that protects you from impulse spending.

How to automate transfers from your checking account to savings

Automation is the single most reliable way to build savings. The pay yourself first method treats your savings transfer like a fixed bill. You pay it before you spend on anything discretionary. This removes willpower from the equation entirely.

Setting up automation takes five straightforward steps:

- Log into your bank’s online portal or mobile app. Most major banks offer a “recurring transfer” or “automatic transfer” feature under the transfers menu.

- Set the destination account. If your savings account is at a different institution, you will need to link it first by providing the routing and account numbers. Verification typically takes 1–2 business days.

- Choose your transfer amount. Start with a figure that represents 5%–10% of your take-home pay if you are new to saving. You can increase it once the habit feels natural.

- Schedule the transfer date. Set it for 1–2 days after your regular payday. Scheduling transfers just after payday reduces the temptation to spend that money first and keeps your checking account liquid for upcoming bills.

- Set up low-balance alerts. Most banking apps let you trigger a text or email when your checking balance drops below a threshold you choose. This early warning prevents overdrafts caused by your automated transfer.

If your employer offers direct deposit splitting, use it. You can instruct payroll to send a fixed dollar amount or percentage directly to your savings account, bypassing checking entirely. This method is even more effective than a bank transfer because the money never appears in your spending account.

Pro Tip: Start your automated transfer at a smaller amount than you think you can afford. After 60 days, increase it by $25–$50. Gradual increases are easier to sustain than large commitments made on motivation alone.

What fees and mistakes can undermine your savings progress?

Fees are the silent drain on any savings plan. Knowing where they hide lets you avoid them before they cost you real money.

The most common pitfalls include:

- Excess withdrawal fees: Many savings accounts still enforce a limit of six withdrawals per month. Exceeding that limit triggers excess withdrawal fees that can easily wipe out a month of interest earnings.

- Monthly maintenance fees: Some accounts charge $5–$15 per month unless you maintain a minimum balance. A $10 monthly fee on an account earning modest interest can produce a net loss.

- Overdraft fees on your checking account: If your automated transfer pulls more than your checking balance holds, you face an overdraft charge. Always leave a buffer of at least $100–$200 in checking before your transfer date.

- Low-rate inertia: Leaving money in a traditional savings account earning as little as 0.38% APY is one of the most common and costly mistakes savers make. That rate barely keeps pace with anything.

Keeping your savings at a separate institution introduces deliberate friction. When funds are not one tap away, you are far less likely to dip into them for non-emergencies. This behavioral guardrail works better than any budgeting app because it operates at the account structure level, not the willpower level.

Reading the fine print on any account before you open it is non-negotiable. Rate Grove’s guide on reading fee disclosures walks you through exactly what to look for in a bank’s account agreement. Fees buried in disclosures are just as real as the ones advertised upfront.

How do you maximize returns beyond a basic savings account?

A basic savings account gets you started, but it is rarely the best long-term home for your money. The gap between a standard savings account and a high-yield savings account is significant enough to matter over months and years.

The table below compares the three main account types on the factors that affect your net return:

| Feature | Standard savings | High-yield savings | Money market |

|---|---|---|---|

| Typical APY | Near 0.38% | Significantly higher | Moderate |

| Monthly fees | Varies | Often none | Varies |

| Minimum balance | Low | Low to moderate | Often higher |

| Withdrawal access | Limited | Limited | More flexible |

| Best use | Emergency buffer | Primary savings | Accessible savings |

Shopping for rates matters more than most people realize. Savings rates differ widely by bank, and sticking with your default checking bank out of convenience often means leaving money on the table. Online banks consistently offer higher APYs because they do not carry the cost of physical branches.

High APY alone is not the full picture. Net returns depend on fees and account conditions, not just the advertised rate. An account paying 4.5% APY with a $15 monthly maintenance fee may actually underperform a 4.0% APY account with no fees, depending on your balance.

Set a calendar reminder every six months to review your savings account rate. Banks adjust rates frequently, and an account that led the market in january may be average by july. Staying current on rates is one of the simplest ways to maximize high-yield savings contributions without changing your behavior at all.

Pro Tip: When comparing accounts, calculate your actual monthly interest earnings after fees. Divide the annual APY by 12, multiply by your average balance, then subtract any monthly fees. That number is your real monthly gain.

Key Takeaways

Automating transfers from checking to a dedicated high-yield savings account, while actively avoiding fees and withdrawal limits, is the most reliable path to building savings that actually grow.

| Point | Details |

|---|---|

| Know your savings margin | Calculate monthly income minus fixed expenses before setting any transfer amount. |

| Automate immediately after payday | Schedule transfers 1–2 days post-payday to reduce spending temptation and protect cash flow. |

| Avoid fee traps | Watch for excess withdrawal fees, maintenance charges, and overdraft risks that erode interest gains. |

| Shop for better rates | Traditional savings accounts average as low as 0.38% APY; high-yield accounts pay significantly more. |

| Review accounts every six months | Rates change frequently, so periodic reviews keep your savings working at its best. |

Why simplicity and consistency beat complexity every time

I have spent years watching people build elaborate savings systems that collapse within three months. The ones who actually build wealth do something much simpler: they automate a fixed amount, forget about it, and review it twice a year.

The psychological case for automation is stronger than most people expect. When you remove the decision from your hands, you also remove the guilt, the negotiation, and the “I’ll do it next month” delay. The pay yourself first approach works not because it is clever, but because it is boring. Boring is exactly what savings needs to be.

My honest advice is to start smaller than feels meaningful. A $50 automated transfer feels insignificant, but it builds the habit and the account structure. Once that runs for 60 days without drama, you increase it. The goal in the first quarter is not the balance. The goal is proving to yourself that the system works.

The other thing I have learned is that people underestimate how much fees cost them relative to interest earned. I have seen savers celebrate a 4% APY while paying $12 a month in maintenance fees on a $1,500 balance. That fee alone costs them nearly 10% of their annual interest. Always do the math on net return, not headline rate.

— Mat C.

Rate Grove makes finding the right savings account faster

Finding a savings account that actually fits your goals takes more than a quick search. Rates change monthly, fees hide in fine print, and the account that looks best on the surface often is not once you factor in minimums and withdrawal rules.

Rate Grove compares bank accounts, CD rates, and credit cards side by side using verified data from issuer and regulator sites. Every listing shows fees, APY, and key tradeoffs in one place, so you can evaluate accounts in minutes rather than hours. The guides are updated monthly and fact-checked, which means you are always looking at current rates, not last quarter’s numbers. If you are ready to put your savings in an account that actually earns, Rate Grove is the place to start comparing.

FAQ

What is the best percentage to transfer from checking to savings?

Financial experts recommend saving 5%–20% of take-home pay, starting at the lower end if you are new to saving. Increase the percentage gradually as your budget adjusts.

How long does a transfer from checking to savings take?

Internal transfers at the same bank process instantly. External transfers between institutions take 1–3 business days, so plan around bill due dates.

Can I get charged fees for moving money to savings too often?

Yes. Many savings accounts limit withdrawals to six per month and charge fees for exceeding that limit. Check your account’s terms before setting up frequent automated transfers.

Why does my savings account earn so little interest?

Traditional savings accounts average as low as 0.38% APY. Switching to a high-yield savings account at an online bank is the fastest way to earn meaningfully more on the same balance.

Should I keep my savings at the same bank as my checking account?

Keeping savings at a separate institution reduces impulse withdrawals by adding friction to the process. That small inconvenience protects your savings from being spent on non-essentials.