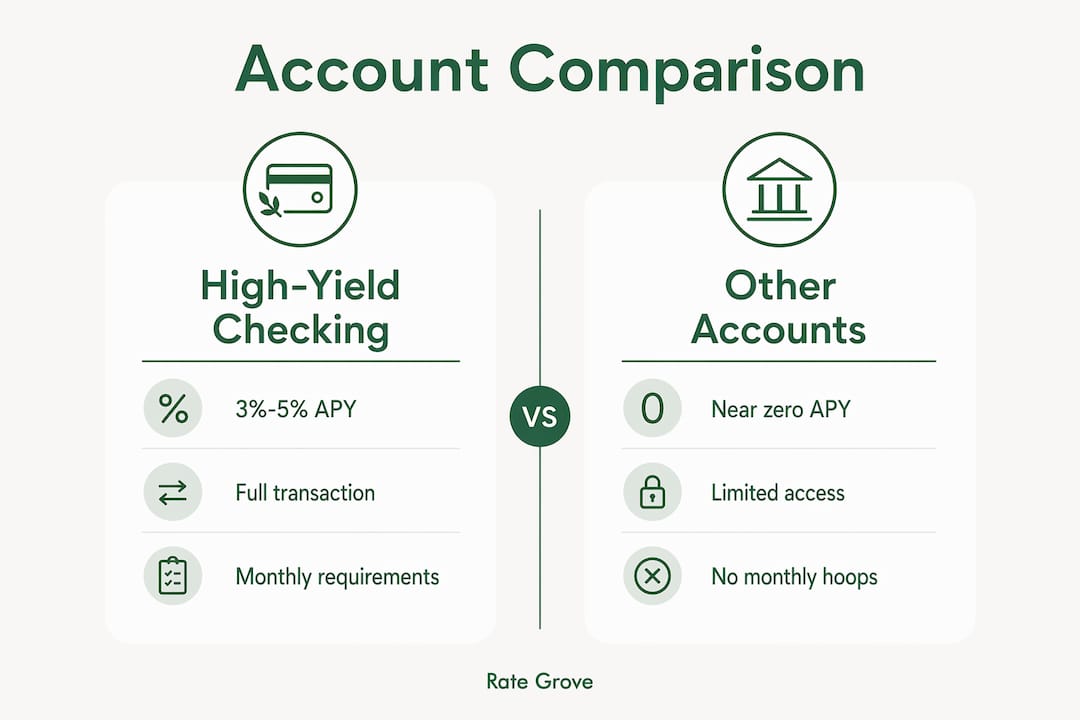

A high-yield checking account is defined as a standard checking account that pays a significantly higher annual percentage yield (APY) than a typical bank account, often between 3% and 5% or more, provided you meet specific monthly criteria. The industry term for this product is a “rewards checking account” or “high-interest checking account,” and both names describe the same core concept. As of march 2026, average checking accounts pay just 0.07% APY, while high-yield versions can pay over 40 times that rate. That gap represents real money sitting idle in accounts that could be working harder for you every month.

What is a high-yield checking account and how does it work?

A high-yield checking account functions like any regular checking account. You can pay bills, use a debit card, make transfers, and withdraw cash without restriction. The key difference is that it earns interest on your balance while giving you full access to your money, unlike some savings accounts that cap monthly withdrawals.

The interest is typically calculated daily and credited to your account monthly. Most accounts use a tiered APY structure, meaning the top rate applies only up to a set balance cap. Balance caps often fall between $10,000 and $25,000. Any amount above that cap earns a much lower rate, sometimes close to zero.

Monthly qualifying requirements

To earn the advertised rate, you must meet a checklist of monthly activities. These requirements vary by bank, but the most common ones include:

- Minimum debit card transactions: Most accounts require 10 to 15 debit card purchases per month.

- Direct deposit: A qualifying paycheck or government payment deposited electronically each month.

- E-statements: Enrolling in paperless statements is a standard prerequisite at many banks.

- Online bill pay: Some banks require at least one bill paid through their online portal.

- Minimum balance: A few accounts set a daily or monthly average balance floor.

Missing these monthly criteria causes your APY to drop sharply, often to near zero, for that entire statement cycle. This surprises many account holders who assume the rate is automatic.

Pro Tip: Set a calendar reminder three days before your statement cycle closes. Check your transaction count and direct deposit status so you never miss the qualifying threshold.

How do high-yield checking accounts compare to other account types?

Choosing between a high-yield checking account, a traditional checking account, and a high-yield savings account depends on how you use your money day to day. Each account type serves a different purpose.

Traditional checking accounts offer near-zero interest but no hoops to jump through. High-yield savings accounts, by contrast, often pay competitive APYs without monthly transaction requirements. However, high-yield checking accounts create passive income on money you spend daily, which is something a savings account cannot replicate for your spending funds.

The table below outlines the key differences across all three account types.

| Feature | Traditional checking | High-yield checking | High-yield savings |

|---|---|---|---|

| Typical APY | ~0.07% | 3%–5%+ (with requirements) | 4%–5% (varies) |

| Monthly transaction limits | None | None | May be limited |

| Qualifying requirements | None | Yes (debit use, direct deposit) | Usually none |

| Balance cap for top rate | N/A | $10,000–$25,000 typically | Varies |

| Best use | Daily spending | Daily spending + interest | Saving and growing funds |

| Liquidity | Full | Full | Full but sometimes restricted |

The clearest takeaway from this comparison: a high-yield savings account often wins for money you plan to leave untouched. A high-yield checking account wins for money you spend regularly, because it earns interest on funds that would otherwise sit idle in a zero-rate account. For a deeper look at types of savings accounts, Rate Grove covers the full range of options with verified rate data.

What are the drawbacks of high-yield checking accounts?

High-yield checking accounts carry real limitations that the advertised APY does not reveal upfront. Understanding these before you open an account protects your earnings and your time.

The biggest risk is rate volatility tied to your behavior. Failing to meet monthly activity requirements resets your interest rate to near zero for that cycle. One missed month of debit card swipes can wipe out weeks of earned interest.

Other drawbacks worth knowing:

- Teaser rates: Some banks advertise promotional APYs that drop after an introductory period. Chasing the highest APY without reading the fine print often leads to disappointment.

- Balance caps: Earning 4% on only the first $10,000 of a $30,000 balance means the effective yield on your total balance is much lower than advertised.

- Tax liability: Interest earned in a checking account is taxable income. Your bank will issue a 1099-INT form if you earn more than $10 in interest during the year.

- Monthly fees: Some accounts charge maintenance fees that can offset interest earnings if you do not meet minimum balance or activity thresholds.

- Complexity: Tracking debit card swipes and direct deposit deadlines adds a layer of management that a traditional account does not require.

Pro Tip: Before opening any account, read the full account disclosure document. Account disclosures are the only legally binding source for fee triggers, rate drop conditions, and balance requirements. Many people skip this step and pay for it later.

Understanding how bank fees drain savings is equally important. A fee of $12 per month erases roughly $144 per year, which can cancel out interest earned on a modest balance.

How to choose the best high-yield checking account for your needs

Selecting the right account starts with an honest look at your own banking habits. The best rate on paper means nothing if you cannot consistently meet the requirements to earn it.

-

Audit your monthly transactions. Count how many debit card purchases you make in a typical month. If you rarely use a debit card, an account requiring 15 monthly swipes will be difficult to maintain.

-

Confirm your direct deposit setup. Most high-yield checking accounts require a qualifying direct deposit. Verify that your employer’s payroll system can route funds to a new account before switching.

-

Compare APYs alongside balance caps. A 5% APY capped at $10,000 earns $500 per year on that portion. A 4% APY capped at $25,000 earns $1,000. The lower rate can produce higher total earnings depending on your balance.

-

Review the fee schedule carefully. Look for monthly maintenance fees, out-of-network ATM fees, and minimum balance penalties. Some accounts reimburse ATM fees nationwide, which adds real value for frequent cash users.

-

Check for e-statement and online bill pay requirements. Digital banking habits like paperless statements and online bill pay are prerequisites at many banks. If you prefer paper statements, confirm whether opting out disqualifies you from the high rate.

-

Use a comparison tool. Rate Grove compiles verified rate comparisons across banks so you can evaluate APYs, fees, and requirements side by side without hunting through individual bank websites.

Experts agree that high-yield checking accounts work best for money you access frequently, not for long-term savings or investment funds. Align the account to your actual spending patterns, and the interest takes care of itself.

Key takeaways

A high-yield checking account earns 3%–5% APY on everyday spending money, but only when you consistently meet monthly qualifying requirements like debit card use and direct deposit.

| Point | Details |

|---|---|

| Definition | A checking account paying 3%–5% APY, far above the 0.07% national average. |

| Qualifying requirements | Monthly debit transactions, direct deposit, and e-statements are standard criteria. |

| Balance caps | The top rate typically applies only to the first $10,000–$25,000 in the account. |

| Missed requirements | Failing monthly criteria drops your APY to near zero for that entire cycle. |

| Best use case | Everyday spending money, not long-term savings or large parked balances. |

The rate is only as good as your habits

I have reviewed hundreds of bank accounts over the years, and high-yield checking accounts are one of the most misunderstood products in personal finance. People see a 4% or 5% APY and assume it works like a savings account. It does not. The rate is conditional, and the conditions are behavioral.

The readers who get the most out of these accounts are not necessarily the ones with the highest balances. They are the ones who already use a debit card regularly, already receive direct deposit, and already prefer paperless statements. For them, the account requires almost no extra effort. The interest just shows up.

Where I see people go wrong is in opening an account for the rate alone, without checking whether their habits match the requirements. They earn the high yield for one or two months, then miss a requirement in a busy month, and the interest disappears. That cycle is frustrating and avoidable.

My honest advice: treat a high-yield checking account as a tool for your spending money, not a replacement for a dedicated savings strategy. Use it for the funds you cycle through every month. Keep your longer-term savings in a separate account built for growth. The two products complement each other well when you use each one for its intended purpose.

— Mat C.

Find the right account without the guesswork

Comparing high-yield checking accounts across banks takes time when you have to visit each bank’s website separately, cross-reference fee schedules, and verify whether rates are promotional or permanent.

Rate Grove does that work for you. The platform pulls verified rate and fee data from issuer and regulator sources, then presents bank accounts, CDs, and credit cards side by side so you can compare what actually matters: APY, balance caps, monthly requirements, and fees. Every guide on Rate Grove is updated monthly, so the numbers you see reflect current offers, not last year’s promotions. If you are ready to find an account that fits your habits and your balance, Rate Grove is the place to start.

FAQ

What is the difference between a high-yield checking and savings account?

A high-yield checking account offers full transaction access with no withdrawal limits, while a high-yield savings account is designed for funds you leave untouched. Checking accounts require monthly activity to earn the top rate; savings accounts typically do not.

What APY can I expect from a high-yield checking account?

Most high-yield checking accounts offer between 3% and 5% APY when you meet monthly requirements, compared to the national average of 0.07% for standard interest-bearing checking accounts.

What happens if I miss the monthly requirements?

Missing qualifying criteria, such as debit card transactions or direct deposit, causes your APY to drop to near zero for that statement cycle. You do not lose existing interest already credited, but you forfeit earnings for the month you miss.

Are high-yield checking accounts FDIC insured?

Yes. High-yield checking accounts at FDIC-member banks are insured up to $250,000 per depositor, per institution, per ownership category, the same protection that covers traditional checking accounts.

Is interest from a high-yield checking account taxable?

Yes. The IRS treats interest earned in a checking account as ordinary income. Your bank will send a 1099-INT form if you earn more than $10 in interest during the tax year.