Monthly fees are charges banks impose for maintaining your checking or savings account each billing cycle. Understanding how banks calculate monthly fees is the fastest way to stop paying for something you can avoid. Banks primarily use two balance methods, average daily balance and minimum daily balance, to decide whether to charge or waive your fee. Monthly maintenance fees typically range from $5 to $35 per month, which adds up to $60 to $300 annually if you never meet the waiver conditions. The Consumer Financial Protection Bureau (CFPB) requires banks to disclose these fees clearly, but the calculation mechanics behind them remain poorly understood by most account holders.

How banks calculate monthly fees using daily and monthly balances

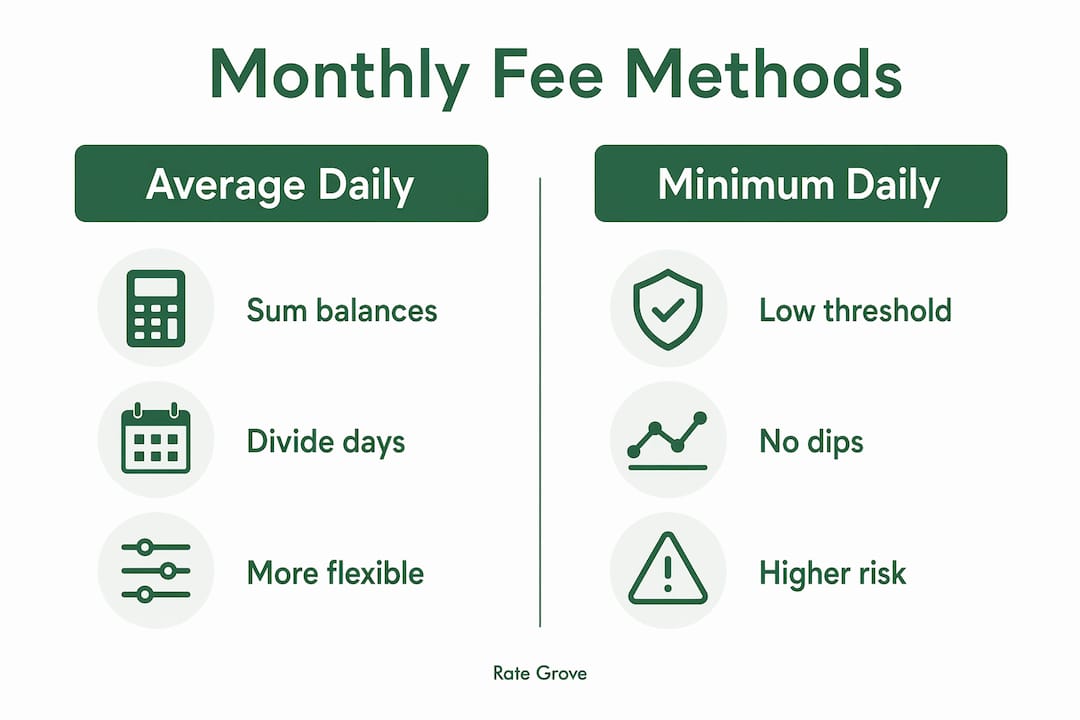

Banks calculate your monthly fee by measuring your account balance against a threshold they set in your account agreement. The industry term for this process is “balance-based fee assessment,” and it uses one of two methods: average daily balance or minimum daily balance.

Average daily balance

The average daily balance is calculated by recording your end-of-day balance for every calendar day in the statement cycle, summing all those figures, and dividing by the number of days in that cycle. Statement cycles run 28 to 31 days depending on the month and the bank. If your cycle has 30 days and your daily balances sum to $15,000, your average daily balance is $500.

This method gives you flexibility. You can dip below the threshold on some days as long as your average recovers by the end of the cycle. That flexibility is the key difference between this method and the minimum daily balance approach.

Minimum daily balance

The minimum daily balance method requires your account balance to never fall below the threshold on any single day during the cycle. One low day triggers the full fee, regardless of how high your balance was on every other day. Banks specify which method applies to fee waivers versus interest calculations, and these rules are not always the same within the same account.

The table below summarizes how each method works in practice.

| Method | How it works | Risk level |

|---|---|---|

| Average daily balance | Sum all end-of-day balances, divide by cycle days | Lower: temporary dips are allowed |

| Minimum daily balance | Balance must stay above threshold every single day | Higher: one low day triggers the fee |

| Average monthly balance | Similar to average daily but calculated over a calendar month | Moderate: depends on bank’s cycle definition |

Pro Tip: Check your account agreement’s fee schedule summary for the exact phrase “average daily balance” or “minimum daily balance.” These two terms are not interchangeable, and your bank’s choice directly determines how much buffer you actually have.

What are typical monthly fee ranges and waiver conditions?

Monthly maintenance fees average around $14 for standard checking accounts, with a range of $5 to $35 depending on the account tier and institution. That average figure matters because it means most people paying a fee are not paying the maximum. They are paying a mid-range amount that feels small monthly but costs over $160 per year.

Large national banks typically require one of the following to waive the fee:

- A qualifying direct deposit of $250 to $1,000 per month

- A minimum or average balance of $500 to $1,500

- A combined balance across linked accounts (often $1,500 or more)

- Age-based waivers for students under 24 or seniors over 65

- Relationship-based waivers tied to holding a mortgage or investment account

Major banks such as Chase and Bank of America typically require a $1,500 combined or average balance to waive fees on standard checking accounts. That threshold is not negotiable at the teller window. It is set by the account product itself.

Online-only banks take a different approach entirely. As of 2026, most charge no monthly maintenance fees and impose no minimum balance requirements. This is not a promotional offer. It reflects a structural cost advantage: online banks carry no branch network overhead, so they pass those savings directly to account holders.

One detail that catches many people off guard: fees are not prorated. If your balance falls even one cent below the required threshold on the wrong day or in the wrong average, the bank charges the full fee for the entire month. There is no partial charge for the days you were below.

Pro Tip: Focus on qualifying direct deposits first, not balance maintenance. A single payroll deposit that meets the threshold is more reliable than trying to keep a precise daily balance.

Why do banks charge monthly fees at all?

Banks charge monthly fees to cover the real operational costs of running your account. These costs include branch infrastructure, customer service staffing, fraud monitoring systems, regulatory compliance, and check processing. A low-balance account that holds $200 generates almost no net interest income for the bank. The fee covers the gap.

The operational expenses covered by monthly fees typically include:

- Physical branch networks and ATM maintenance

- 24/7 customer support centers

- Fraud detection and prevention technology

- Federal regulatory compliance and reporting

- Core banking system infrastructure

Banks design monthly fees and waivers to reward customers with consistent payroll deposits or higher balances. Accounts with low liquidity are effectively penalized because they cost the bank more to service than they generate in revenue.

“Monthly fees are not arbitrary. They reflect the real cost of maintaining an account that generates little or no interest income for the bank. Understanding that logic helps you negotiate from a position of knowledge, not frustration.”

This perspective from financial educators highlights something most consumers miss: the fee is a product design choice, not a penalty. Banks build fee waivers into accounts specifically to attract customers who bring consistent deposit activity. If you meet those criteria, the fee disappears. If you do not, you are subsidizing the bank’s cost to serve you.

Reviewing the fee schedule summary in your account agreement reveals not just the monthly fee but also secondary charges like paper statement fees, overdraft fees, and wire transfer costs. These secondary fees can add hundreds of dollars annually on top of the base monthly charge.

How to monitor and avoid monthly banking fees

Avoiding monthly fees starts with knowing exactly which calculation method your bank uses and then building habits around it. The steps below apply regardless of which bank or account type you hold.

- Log into your online banking portal weekly. Check your running balance against the fee threshold. Most banks display your current average daily balance in the account details section.

- Set low-balance alerts. Configure text or email alerts to notify you when your balance drops within $100 of the threshold. This gives you time to transfer funds before the cycle closes.

- Confirm what counts as a qualifying direct deposit. Qualifying deposits include payroll, government benefits, and pensions. Personal transfers from another bank account or payments from apps like Venmo or Zelle typically do not count. Call your bank and ask them to confirm in writing.

- Explore age-based or relationship waivers. If you are a student, a senior, or you hold a mortgage with the same bank, you may qualify for a fee waiver you have never applied for.

- Consider switching to an online bank. Online banks eliminate monthly fees entirely by operating without branch overhead. If you rarely visit a physical branch, the switch costs you nothing and saves you up to $300 per year.

- Call customer service if a fee posts unexpectedly. Banks will often reverse a fee once, especially for long-standing customers. Ask directly: “Can you reverse this fee and explain which waiver condition I missed?”

Pro Tip: Ask your bank’s customer service representative to walk you through the exact waiver conditions on your specific account. Product names change, and the waiver rules on your account may differ from what the bank advertises for new customers today.

Understanding fee disclosure tables is the single most underused tool for avoiding charges. Banks are required to provide these documents, but most account holders never read them past the first page.

Key Takeaways

Banks calculate monthly fees using either average daily balance or minimum daily balance methods, and missing the threshold by even one cent triggers the full charge with no proration.

| Point | Details |

|---|---|

| Two balance methods | Banks use average daily balance or minimum daily balance; know which one your account uses. |

| Fee range | Monthly fees run $5–$35, averaging around $14; unchecked, they cost up to $300 per year. |

| Qualifying deposits matter | Only payroll, government benefits, and pensions count as qualifying direct deposits for most waivers. |

| No proration rule | A balance one cent below threshold triggers the full monthly fee regardless of other days. |

| Online banks charge zero | Most online-only banks carry no monthly fees and no minimum balance requirements as of 2026. |

What I’ve learned after years of watching people pay fees they shouldn’t

The single most common mistake I see is people confusing average daily balance with minimum daily balance. They assume that keeping their account above $1,500 for most of the month is enough. Then they get hit with a $14 fee because their balance dipped to $1,499 on one Tuesday after a bill posted. That confusion costs American consumers real money every month.

The second mistake is assuming that moving money from a savings account into checking counts as a qualifying direct deposit. It does not. Banks are very specific about this, and the definition is buried in the account agreement, not on the product page. I have seen people set up automatic transfers for months, convinced they were meeting the waiver condition, only to find out later that none of those transfers qualified.

The trend toward online banking is the most consumer-friendly shift in retail banking in the past decade. When a bank has no branches to maintain, it has no structural reason to charge a monthly fee. That is not marketing. It is economics. If you are still paying a monthly fee at a traditional bank and you rarely use a branch, the math on switching is straightforward.

My honest advice: read your fee schedule once, set one balance alert, and confirm your direct deposit qualifies. Those three steps take 20 minutes and can save you $168 or more per year. The knowledge is free. The fee is not.

— Mat C.

Find accounts with no monthly fees at Rate Grove

Knowing how banks charge fees is only half the work. The other half is finding an account that fits your actual deposit habits and balance patterns.

Rate Grove compares bank accounts, CDs, and credit cards side by side using verified data from issuer and regulator sites. You can filter by monthly fee, waiver conditions, and minimum balance requirements to find accounts that match how you actually bank. Every listing is updated monthly, so you are not comparing outdated terms. Compare bank accounts and fees at Rate Grove and find a product that works for your balance, not against it.

FAQ

How do banks calculate monthly fees?

Banks calculate monthly fees by measuring your account balance against a set threshold using either the average daily balance or minimum daily balance method. If your balance does not meet the threshold, the bank charges the full monthly fee with no proration.

What is the average monthly bank fee in 2026?

Monthly maintenance fees average around $14 for standard checking accounts, with a range of $5 to $35 depending on the bank and account tier.

Does a bank transfer count as a qualifying direct deposit?

Personal transfers from another bank account or P2P payment apps do not qualify as direct deposits for fee waiver purposes. Only payroll, government benefits, and pension payments typically meet the definition.

What happens if my balance drops below the threshold for one day?

If your balance falls below the required threshold even once during the cycle (under the minimum daily balance method), the bank charges the full monthly fee for that entire month. There is no partial or prorated charge.

Do online banks charge monthly maintenance fees?

Online-only banks generally charge no monthly maintenance fees and require no minimum balance as of 2026, making them a practical option for consumers who want to avoid recurring account charges.