High-yield savings for irregular income is the practice of routing variable earnings through specialized accounts to earn competitive interest while maintaining financial stability. Freelancers, gig workers, and self-employed individuals face a problem that salaried workers never encounter: income that swings wildly from month to month. The solution is a structured 3-account system endorsed by financial experts, which separates holding funds, tax obligations, and spending money into distinct accounts. Top-tier high-yield savings accounts currently offer APYs near 5.00%, making the interest earned on your buffer genuinely meaningful.

How to calculate your baseline income and survival budget

Your baseline monthly income is the foundation of every savings decision you make. Without it, you are guessing, and guessing leads to overdrafts and stress.

The most reliable method is to average your three lowest-earning months from the past 12 months. That number becomes your “survival income,” the conservative floor you plan around. Using your best months as a baseline is the most common mistake variable earners make. It sets expectations too high and leaves you short when work slows down.

Once you have your survival income, calculate your total essential monthly expenses. This means:

- Housing (rent or mortgage, including renter’s or homeowner’s insurance)

- Utilities (electricity, gas, water, internet)

- Food (groceries only, not dining out)

- Health insurance and any required medications

- Minimum debt payments (student loans, car payment)

Add those five categories together. That total is your survival number, the minimum you need each month to keep your life running. Every savings and tax decision you make should protect that number first.

Your buffer target is 3–6 months of your survival number. That range gives you a cushion for slow seasons, client payment delays, or unexpected expenses without touching a credit card. Building to that range takes time, and the next section explains exactly how to get there.

Pro Tip: Write your survival number on a sticky note and keep it visible. Knowing it by heart prevents impulsive spending during a good month.

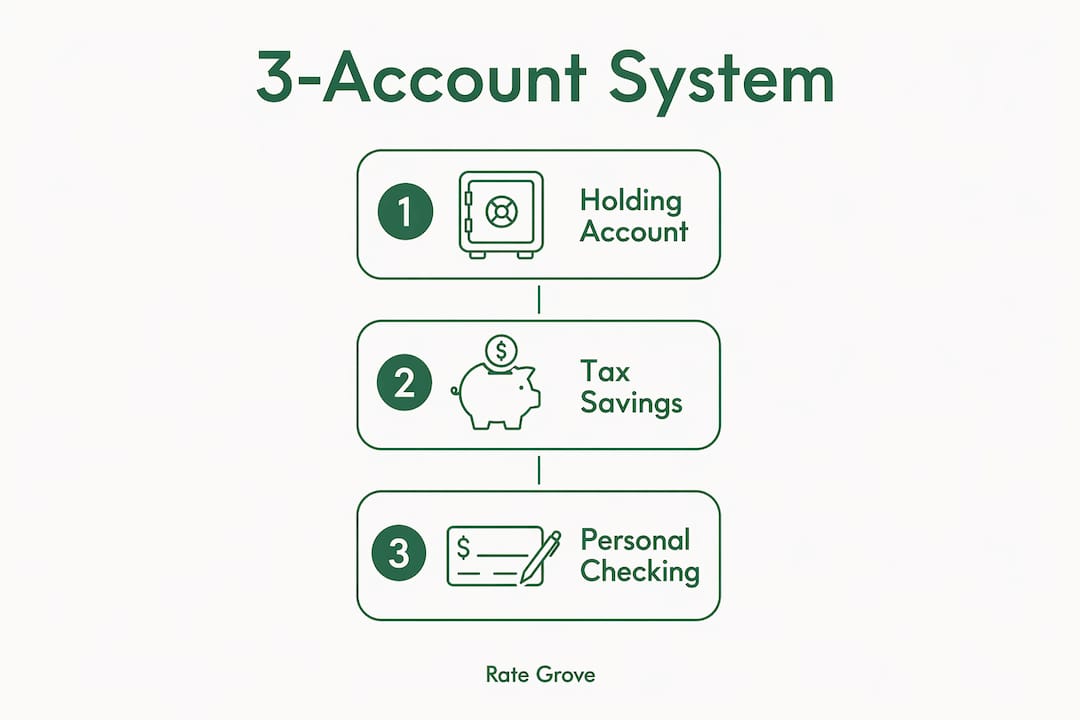

What is the 3-account system for variable income?

The 3-account system is the most effective structure for managing high-yield savings with irregular income. Each account has one job, and money flows in a specific direction.

Account 1: The high-yield holding account

All income lands here first. Every client payment, every gig payout, every invoice goes directly into this account. The holding account acts as a buffer between your unpredictable earnings and your actual spending. You want a no-fee, no-minimum-balance high-yield savings account here so that even during a slow month with a low balance, you pay nothing.

Account 2: The tax savings account

The moment money hits your holding account, transfer 25–30% of that deposit to a dedicated tax savings account. This is non-negotiable for 1099 income. The IRS expects quarterly estimated tax payments, and failing to make them triggers penalties. Keeping tax money in the same account as your buffer is how freelancers accidentally spend it.

The best practice is to open this tax savings account at a different bank entirely. The one-to-two day ACH transfer delay creates friction that prevents accidental withdrawals. Out of sight genuinely means out of reach.

Account 3: Personal checking account

Once a month, transfer a fixed “salary” from your holding account into your personal checking account. That salary equals your survival number. You spend from checking only. This single habit removes the psychological chaos of variable income because your day-to-day spending feels exactly like a regular paycheck.

Here is how the money flows in practice:

| Step | Action | Account involved |

|---|---|---|

| 1 | Client pays invoice | Holding account (HYSA) |

| 2 | Transfer 25–30% immediately | Tax savings account (HYSA) |

| 3 | Monthly fixed salary transfer | Personal checking account |

| 4 | Remainder stays and earns interest | Holding account (HYSA) |

Pro Tip: Set a recurring calendar reminder on the 1st of each month to make your salary transfer. Automating the decision removes willpower from the equation.

Choosing accounts with flat APY structures matters here. Accounts that require consistent direct deposits to unlock their advertised rate can penalize variable earners. An account offering 4.50% APY with a qualifying direct deposit may drop to 1.20% without one. A flat rate account with no conditions gives you predictable returns regardless of deposit timing.

Best practices for managing your buffer through high and low months

Building and protecting your buffer is where most variable earners either succeed or fail. The system only works if you respect the rules during both feast and famine.

Budgeting for irregular income is less about prediction and more about stability. Sinking funds and buffer accounts do the heavy lifting so you never have to forecast every variable precisely.

Start small. A $1,000 starter buffer is your first goal, not three months of expenses. That initial $1,000 covers minor emergencies without forcing you onto a credit card. Once you hit $1,000, scale to one month of baseline expenses, then two, then the full 3–6 month target.

Follow these rules for slow months:

- Keep tax savings intact. Never borrow from the tax account, even temporarily. The penalty and interest from an underpaid quarterly tax bill will cost more than the short-term relief.

- Reduce discretionary transfers. If your holding account balance drops below two months of your survival number, pause any non-essential savings goals.

- Do not raid the buffer. The holding account buffer is for income gaps, not lifestyle spending. Using it for non-essentials breaks the system.

For strong months, the priority order is equally clear. First, replenish any buffer shortfall from the previous slow period. Second, pay down high-interest debt if you carry any. Third, add to longer-term savings or investment accounts. Extras come last.

Sinking funds are a powerful addition to this system. A sinking fund is a dedicated savings bucket for a known future expense, such as annual insurance premiums, quarterly tax payments, or equipment replacement. Instead of scrambling when the bill arrives, you save a fixed amount each month toward it. Many high-yield savings accounts now offer savings buckets or subaccounts to organize these goals without opening separate accounts.

Pro Tip: Label each savings bucket with its purpose and target amount. Seeing “Tax Q3: $2,400 of $3,000” is far more motivating than a single unnamed balance.

How do you choose the right high-yield savings account for variable income?

Choosing the right account is not about finding the highest advertised APY. It is about finding the highest reliable APY for your actual deposit pattern.

The most important filter is APY structure. Conditional APYs that require direct deposits are a trap for irregular earners. If you cannot guarantee a qualifying deposit every month, you cannot count on that rate. Flat APY accounts deliver consistent returns regardless of when or how much you deposit.

Beyond rate structure, evaluate accounts on these criteria:

- No monthly maintenance fees. A fee charged during a zero-balance month wipes out any interest earned and then some.

- No minimum balance requirement. Your holding account may run low during slow periods. You need an account that does not penalize you for that.

- Subaccounts or savings buckets. Features like these let you organize tax savings, emergency funds, and sinking funds within one account without opening multiple accounts.

- Mobile app quality. You will transfer money frequently. A poor app creates friction in the wrong direction.

- Compounding frequency. Daily compounding earns slightly more than monthly compounding on the same APY. Over a year with a large buffer, the difference adds up.

High advertised APYs can mislead variable earners who do not read the conditions. Always check whether the rate requires a minimum deposit, a minimum balance, or a qualifying direct deposit before opening an account. Rate Grove updates its savings account comparisons monthly with verified data from issuer sites, so you can compare current rates without hunting through outdated information.

Online banks consistently pay more on savings accounts than traditional brick-and-mortar banks because they carry lower overhead costs. For irregular income earners, online banks also tend to offer the no-fee, no-minimum structures that make the 3-account system work cleanly.

Key Takeaways

The most effective approach to high-yield savings with irregular income is a 3-account system that separates holding funds, tax obligations, and spending into distinct accounts earning competitive, flat-rate APYs.

| Point | Details |

|---|---|

| Calculate your survival number | Average your three lowest months from the past year to set a conservative baseline budget. |

| Use the 3-account structure | Route all income to a holding HYSA, transfer 25–30% to a tax account, then pay yourself a fixed monthly salary. |

| Protect tax savings first | Never borrow from the tax account; quarterly IRS penalties cost more than any short-term relief. |

| Choose flat APY accounts | Conditional APYs that require direct deposits can drop sharply when deposits are irregular. |

| Build the buffer incrementally | Start with $1,000, then scale to 1–3 months, then the full 3–6 month target over time. |

Why simplicity is the real secret to saving on irregular income

The biggest mistake I see variable earners make is building a system so complex it collapses under its own weight. Four accounts, five apps, a spreadsheet, and a color-coded calendar sounds thorough. In practice, it creates so much friction that people abandon it after two months and go back to winging it.

The 3-account system works because it is boring. You do the same three things every time money arrives: move the tax cut, wait for the monthly salary transfer, let the rest sit and earn interest. That repetition is the point. Discipline is easier when the decision is already made.

The psychological benefit of paying yourself a fixed salary is genuinely underrated. I have spoken with freelancers who described the moment they started the monthly transfer as the first time in years they felt financially normal. Variable income stops feeling chaotic when your checking account behaves like a paycheck.

The one area where I see people go wrong even after setting up the system correctly is chasing APYs. Switching accounts every time a new promotional rate appears costs you time, risks your tax savings sitting in limbo during a transfer, and often nets you less than the advertised difference. Find a flat-rate account with no fees, confirm it is FDIC insured, and stay put. The rate matters less than the consistency.

— Mat C.

Rate Grove makes finding the right account faster

Picking the right high-yield savings account for a variable income situation requires current, accurate data. Rates change, fee structures shift, and promotional APYs expire.

Rate Grove tracks savings account rates, CD rates, and checking account fees monthly using verified data pulled directly from issuer and regulator sites. You get a clear, side-by-side view of APYs, fee structures, and minimum balance requirements without digging through fine print. For irregular income earners who need flat-rate, no-fee accounts, that clarity saves real money. Visit Rate Grove to compare current high-yield savings accounts and find the right fit for your income pattern today.

FAQ

What is the best savings account structure for irregular income?

The 3-account system is the most effective structure: a high-yield holding account for all income, a separate tax savings account funded at 25–30% of each deposit, and a personal checking account receiving a fixed monthly salary transfer.

How much should I set aside for taxes as a freelancer?

Transfer 25–30% of every deposit immediately to a dedicated tax savings account. This covers federal and state estimated quarterly tax payments for most 1099 earners.

Are conditional APY accounts worth it for gig workers?

Conditional APY accounts that require qualifying direct deposits are unreliable for variable earners. A flat APY account delivers consistent returns regardless of deposit timing or amount.

How large should my savings buffer be?

Start with a $1,000 starter fund, then build to 3–6 months of your baseline monthly expenses. That range covers slow seasons and payment delays without forcing you to use credit.

Do I need to open accounts at different banks?

Keeping your tax savings account at a different bank from your holding account creates a one-to-two day transfer delay. That friction prevents accidental spending of money owed to the IRS.